Printable Colorado Promissory Note Form

Printable Colorado Promissory Note Form

When individuals or entities in Colorado engage in lending and borrowing transactions, the Colorado Promissory Note form becomes a crucial document. Serving as a written agreement, it outlines the terms under which money is borrowed and the payment is to be made from the borrower to the lender. This form specifies the loan amount, interest rate, repayment schedule, and any other terms agreed upon by the parties. Not only does it create a legally binding obligation for the borrower to repay the loan, but it also provides a clear record of the debt, making it an indispensable tool for financial clarity and accountability. Moreover, the Colorado Promissory Note can be either secured, involving collateral as a security for the loan, or unsecured, relying solely on the borrower's promise to pay. Knowing the nuances of this form is essential for anyone involved in lending or borrowing money within the state, ensuring that both parties are protected under Colorado law.

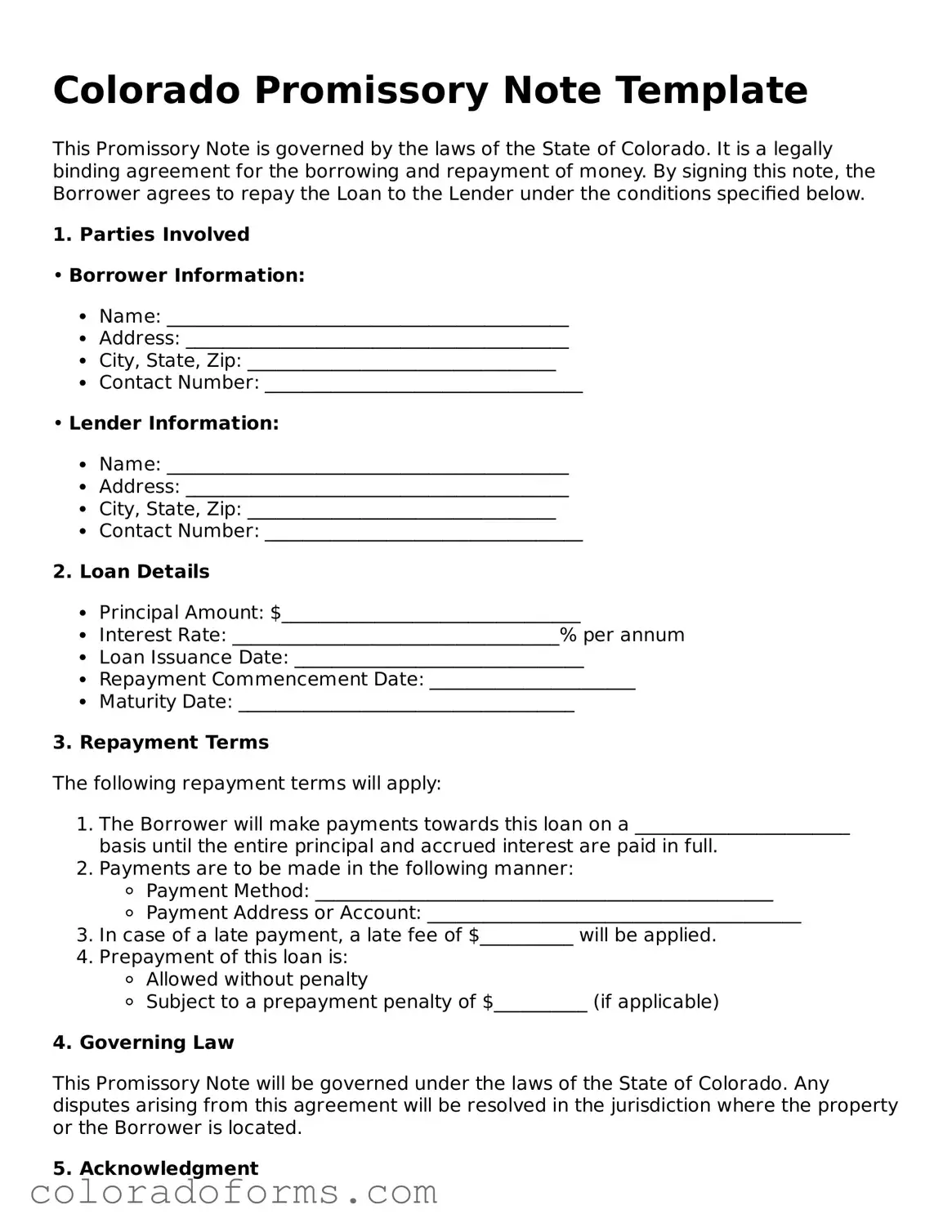

Colorado Promissory Note Template

This Promissory Note is governed by the laws of the State of Colorado. It is a legally binding agreement for the borrowing and repayment of money. By signing this note, the Borrower agrees to repay the Loan to the Lender under the conditions specified below.

1. Parties Involved

• Borrower Information:

• Lender Information:

2. Loan Details

3. Repayment Terms

The following repayment terms will apply:

4. Governing Law

This Promissory Note will be governed under the laws of the State of Colorado. Any disputes arising from this agreement will be resolved in the jurisdiction where the property or the Borrower is located.

5. Acknowledgment

By signing below, both the Borrower and the Lender acknowledge they have read, understood, and agreed to the terms of this Promissory Note.

• Borrower’s Signature: __________________________________ Date: ____________

• Lender’s Signature: ___________________________________ Date: ____________

| Fact | Detail |

|---|---|

| Governing Law | Colorado Revised Statutes |

| Types of Promissory Notes | Secured and Unsecured |

| Requirement for Validity | Must be signed by the borrower |

| Interest Rate Limit | Cannot exceed 45% APR as per Colorado usury laws |

| Prepayment Penalties | Not allowed without prior agreement |

Completing the Colorado Promissory Note form requires attention to detail and an understanding of the information requested. This step-by-step guide is designed to assist in the process, making it more straightforward. The form is a legal document that outlines the details of a loan agreement between two parties. It includes the loan amount, interest rate, repayment schedule, and the obligations of the borrower. After filling out the form, it is critical to review all entered information for accuracy, ensuring that both the lender and borrower agree to the terms before signing. The next steps involve keeping a copy of the signed document for personal records and adhering to the repayment schedule as stipulated.

Upon completion, the signed and dated Colorado Promissory Note form represents a binding legal agreement. It's crucial to adhere to the responsibilities and requirements outlined in the document. Failure to comply with the terms of the promissory note may result in legal consequences for the borrower, including potential claims for the recovery of the loaned amount and other damages.

What is a Colorado Promissory Note?

A Colorado Promissory Note is a legal document that outlines a loan agreement between two parties in the state of Colorado. It details the amount of money borrowed, the repayment schedule, interest rates, and the obligations of both the lender and the borrower. This form is crucial for ensuring that the terms of the loan are clear and legally binding.

Is a written Promissory Note required in Colorado?

While oral agreements can be legally binding, a written Promissory Note is strongly recommended in Colorado. It serves as a physical record of the loan's terms and conditions, which can help prevent disputes and misunderstandings. Furthermore, for loans exceeding a certain amount, Colorado law may require a written agreement for the contract to be enforceable.

What are the key elements that should be included in a Colorado Promissory Note?

A comprehensive Colorado Promissory Note should include the following key elements: the identities of the lender and borrower, the amount of money borrowed, the interest rate, repayment schedule, collateral details (if any), and any applicable late fees or penalties. It should also specify the governing law (Colorado) and include signatures from both parties to acknowledge their agreement to the terms.

How is interest handled on a Promissory Note in Colorado?

In Colorado, the interest rate on a Promissory Note must comply with the state's usury laws, unless a specific exemption applies. The legal maximum interest rate, unless otherwise agreed upon, is set by these laws. If no interest rate is specified in the Promissory Note, Colorado's legal rate of interest, which is established by statute, will apply.

What happens if the borrower fails to repay the loan as agreed?

If the borrower fails to repay the loan according to the terms outlined in the Promissory Note, the lender has the right to pursue legal action to recover the owed amount. This could involve filing a lawsuit to obtain a judgment against the borrower, followed by actions such as garnishing wages or seizing property to satisfy the debt. The specific recourse available may depend on whether the loan is secured by collateral.

Can a Colorado Promissory Note be modified after it has been signed?

Yes, a Colorado Promissory Note can be modified after signing, but any modifications must be agreed upon by both the lender and the borrower. The changes should be documented in writing, and a new Promissory Note or an amendment to the existing note should be executed to reflect the new terms. This ensures that the modifications are legally binding and enforceable.

When filling out a Colorado Promissory Note form, individuals frequently make mistakes that can affect the legality and enforceability of the agreement. It is crucial to approach this document with attention to detail and an understanding of its contents. Here are four common mistakes:

Failing to include specific terms of repayment. Many people overlook the importance of detailing the repayment schedule, interest rates, and due dates. This lack of specificity can lead to misunderstandings and disputes down the line.

Not specifying the interest rate or setting it at a rate that does not comply with Colorado's usury laws. It's essential that the interest rate is clearly defined and lawful to ensure that the note is enforceable and fair to all parties involved.

Omitting collateral terms, if applicable. When a promissory note is secured by collateral, failing to describe the collateral or the conditions under which it can be seized in case of default can create legal ambiguities and complications.

Forgetting to include the signatures of all parties involved. A promissory note must be signed by the borrower and the lender to be legally binding. Any signatory omission can invalidate the document or its enforceability in a court of law.

When preparing a Promissory Note, parties must carefully review and ensure all critical elements are correctly included and accurately described. This diligence helps in protecting the interests of all parties involved and ensures that the agreement holds up legally if ever challenged.

When executing a promissory note in Colorado, several other documents and forms are often used to ensure a comprehensive and legally sound transaction. These documents serve to protect the interests of all parties involved, clarify the terms of the agreement, and provide legal evidence of the commitments made. Each one complements the promissory note by covering additional details or aspects of the financial agreement not covered by the promissory note itself.

Together, these documents form a robust framework supporting the financial transaction detailed in a promissory note. They ensure clarity and security for both parties, minimizing future disputes by detailing every aspect of the agreement and the consequences of non-compliance. While the promissory note itself is crucial, these additional documents are invaluable in reinforcing the agreement's terms and providing clear legal recourse in various scenarios.

The Colorado Promissory Note form is similar to other legal financial agreements designed to confirm and outline the terms of a loan between parties. It shares similarities with documents such as Personal Loan Agreements and IOUs, in the way it specifies the amount borrowed, the repayment schedule, interest rates, and the responsibilities of each party. Each of these documents serves as a legally binding agreement to ensure that the borrower repays the borrowed amount under the agreed-upon terms.

Personal Loan Agreements: This document is closely related to the Colorado Promissory Note in its purpose and content. It details the loan's terms and conditions, including the loan amount, interest rate, repayment schedule, and any collateral involved. The main difference lies in its detailed nature, often incorporating clauses on late fees, dispute resolution methods, and the legal recourse available to the lender if the borrower fails to make payments as agreed. Personal Loan Agreements are more comprehensive and may also include the signatures of witnesses to strengthen the document's legal enforceability.

IOUs: An IOU (I Owe You) is a simpler version of a promissory note. It acknowledges that a debt exists and specifies the amount owed. Unlike the Colorado Promissory Note and Personal Loan Agreements, an IOU typically lacks detailed terms such as repayment schedules, interest rates, and collateral. It serves as a basic acknowledgment of debt between two parties but may not be as enforceable in a court due to the lack of detailed terms. IOUs are often used for informal loans between friends and family members.

Filling out a Colorado Promissory Note requires careful attention to detail and a clear understanding of your obligations. By following some key dos and don'ts, borrowers and lenders can ensure the document is legally sound and reflects the agreed-upon terms. Here are crucial points to consider:

By paying close attention to these do's and don'ts, you can fill out the Colorado Promissory Note form accurately and effectively, providing a secure foundation for the lending agreement. Remember, a well-prepared promissory note not only clarifies the terms of the loan but also serves as a crucial document in the event of a dispute.

Understanding the Colorado Promissory Note form is crucial for individuals and entities engaging in loan agreements within this state. Several misconceptions exist regarding this document, which might lead to confusion or misinterpretation. By clarifying these misconceptions, parties can engage in transactions with a clearer understanding of their rights and obligations.

Clearing up these misconceptions helps both borrowers and lenders approach Colorado Promissory Notes with a better understanding and confidence, facilitating smoother financial transactions and reducing potential legal complications.

When filling out and using the Colorado Promissory Note form, individuals embark on a formal process to document a loan agreement between two parties. Here are several key takeaways to ensure the process is handled accurately and effectively.

Understand the Types: Colorado offers both secured and unsecured promissory notes. Secured notes require collateral, while unsecured ones do not. Choose based on the risk and relationship between the lender and borrower.

Identify the Parties Clearly: Clearly state the names and addresses of the borrower and lender. Precision here is crucial for the legal enforceability of the document.

Amount and Interest: The principal loan amount and the interest rate must be explicitly mentioned. In Colorado, interest rates are subject to state usury laws, so ensure compliance to avoid legal complications.

Repayment Schedule: Detail how the repayment will occur—lump sum, over time with regular payments, etc. This section should include due dates and any grace period for late payments.

Include Late Fees: If there will be penalties for late payments, specify the fee amounts and the conditions under which they are applied. This clarity can prevent disputes down the line.

Security Agreement: For secured notes, describe the collateral that will secure the loan. Be as specific as possible to avoid ambiguity in case of default.

Governing Law: State that Colorado law governs the note. This is important for legal enforcement and resolving any disputes.

Signatures: Both the borrower and the lender must sign the note. For added legal strength, consider having the signatures notarized.

Witnesses or Notarization: Although not always mandatory, having witnesses or notarizing the document can add a layer of verification and authenticity to the agreement.

Keep Copies: Ensure both the borrower and the lender retain copies of the signed note for their records. This aids in maintaining transparent records of the agreement.

Adhering to these guidelines when filling out the Colorado Promissory Note form will help ensure the agreement is clear, enforceable, and complies with applicable laws. Both parties should review the document carefully before signing to ensure all terms are understood and agreed upon.

Colorado New Hire Reporting - Protocols for emergency situations, providing clear instructions to safeguard employees and company assets.

Is Colorado a Marital Property State - Key in protecting personal financial interests and establishing a clear path forward after the divorce.

Letter of Intent to Homeschool Colorado - It is the first legal document that prospective homeschooling parents submit to withdraw their child from public or private school.