Fill a Valid Dr 1083 Colorado Form

Fill a Valid Dr 1083 Colorado Form

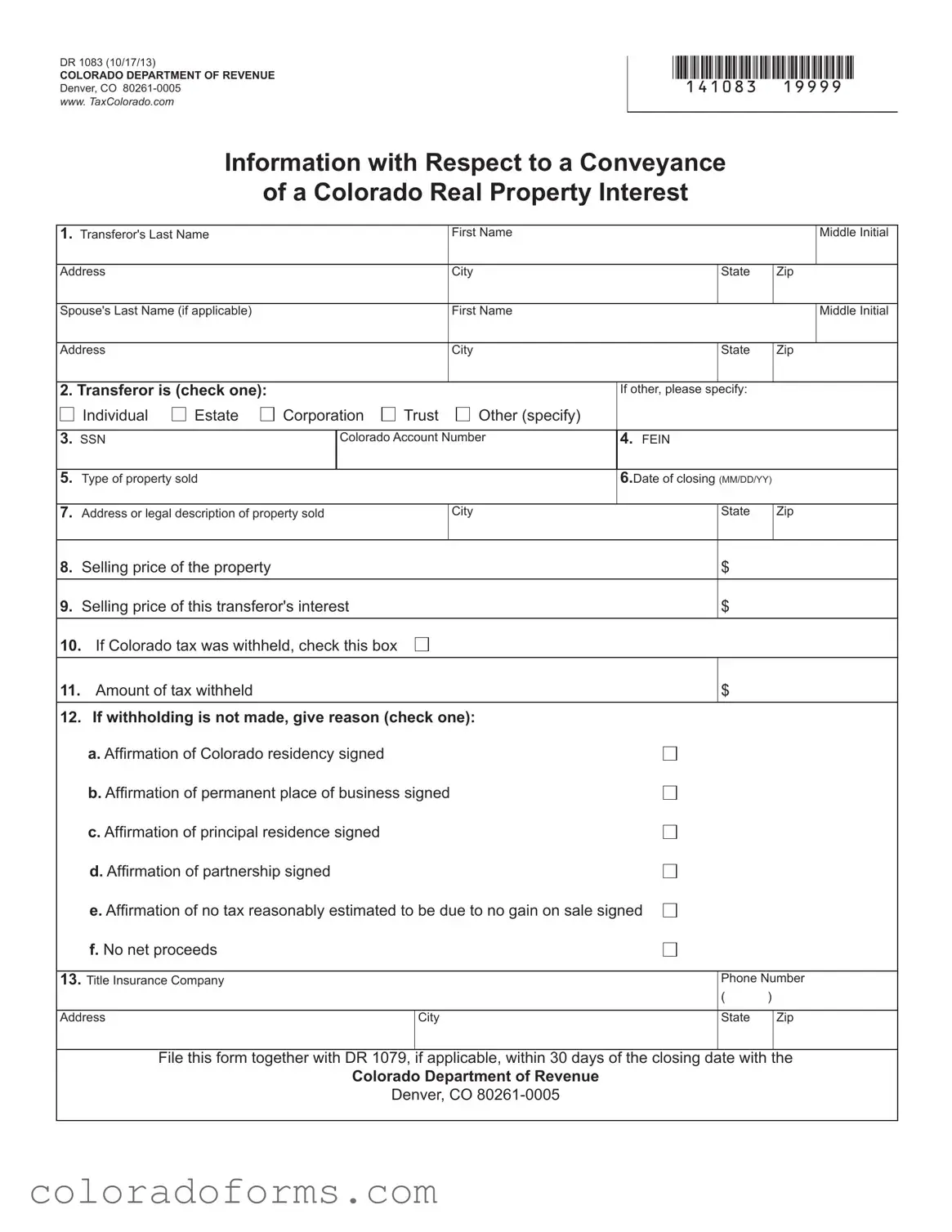

When navigating the complexities of real estate transactions in Colorado, the Dr 1083 form plays a pivotal role, especially for those entangled with the conveyance of a Colorado real property interest. Officially titled "Information with Respect to a Conveyance of a Colorado Real Property Interest," this document serves as a critical tool to ensure compliance with state tax withholding requirements on property sales exceeding $100,000—when the seller is a nonresident or lacks a permanent place of business within the state. Detailed within the form are sections designed to capture essential information about the transferor, including name, address, and the nature of the transferor's interest in the property, alongside specifics of the property itself such as type, selling price, and closing date. Importantly, the form addresses whether Colorado tax has been withheld from the sale proceeds and outlines scenarios under which withholding might not be required, providing a safety net to ensure accurate tax practices. Signatures under penalty of perjury affirm the veracity of claims regarding residency, principal residence status, corporate business presence, or the lack of estimated tax due on the gain from the sale. Intertwined with the procedures for completion and submission—including a necessary accompaniment by form DR 1079 if tax was withheld—the Dr 1083 offers a comprehensive framework for managing the fiscal responsibilities that accompany the transfer of real estate ownership in Colorado.

DR 1083 (10/17/13)

COLORADO DEPARTMENT OF REVENUE

Denver, CO

WWW. TAXCOLORADO.COM

*141083==19999*

Information with Respect to a Conveyance

of a Colorado Real Property Interest

1. Transferor's Last Name |

|

|

|

|

|

First Name |

|

|

|

|

Middle Initial |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

City |

|

State |

|

Zip |

||

|

|

|

|

|

|

|

|

|

|

|

|

||

Spouse's Last Name (if applicable) |

|

|

|

|

|

First Name |

|

|

|

|

Middle Initial |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

City |

|

State |

|

Zip |

||

|

|

|

|

|

|

|

|

|

|

|

|

||

2. Transferor is (check one): |

|

|

|

|

|

|

If other, please specify: |

|

|

|

|||

|

Individual |

Estate |

Corporation |

Trust |

Other (specify) |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

3. |

SSN |

|

|

Colorado Account Number |

4. FEIN |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||

5. |

Type of property sold |

|

|

|

|

|

|

6.Date of closing (MM/DD/YY) |

|||||

|

|

|

|

|

|

|

|

|

|

||||

7. |

Address or legal description of property sold |

|

|

|

City |

|

State |

|

Zip |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

Selling price of the property |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

9. |

Selling price of this transferor's interest |

|

|

|

|

|

$ |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

10. If Colorado tax was withheld, check this box |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|||

11. Amount of tax withheld |

|

|

|

|

|

|

|

$ |

|

|

|

||

|

|

|

|

|

|

|

|||||||

12. If withholding is not made, give reason (check one): |

|

|

|

|

|

||||||||

|

a. Afirmation of Colorado residency signed |

|

|

|

|

|

|

|

|

|

|||

|

b. Afirmation of permanent place of business signed |

|

|

|

|

|

|

||||||

|

c. Afirmation of principal residence signed |

|

|

|

|

|

|

|

|

|

|||

|

d. Afirmation of partnership signed |

|

|

|

|

|

|

|

|

|

|||

|

e. Afirmation of no tax reasonably estimated to be due to no gain on sale signed |

|

|

|

|||||||||

|

f. No net proceeds |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

13. Title Insurance Company |

|

|

|

|

|

|

|

Phone Number |

|||||

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Address |

|

|

|

|

City |

|

|

State |

|

Zip |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

File this form together with DR 1079, if applicable, within 30 days of the closing date with the

Colorado Department of Revenue

Denver, CO

*141083==29999*

Afirmation of Colorado Residency

I (we) hereby afirm that I am (we are) the transferor(s) or the iduciary of the transferor of the property described on this

DR 1083 and that as of the date of closing I am (we are) or the estate or the trust is a resident of the State of Colorado.

Signed under the penalty of perjury

Signature of transferor or iduciary

Date (MM/DD/YY)

Spouse's signature (if applicable)

Date (MM/DD/YY)

Afirmation of Permanent Place of Business

I hereby afirm that the transferor of the property described on this DR 1083 is a corporation which maintains a

permanent place of business in Colorado.

Signed under the penalty of perjury.

Signature of corporate oficer

Date (MM/DD/YY)

Afirmation of Sale by Partnership

I hereby afirm that the transfer of property described on this DR 1083 was sold by an organization deined as a partnership under section 761(a) of the Internal Revenue Code and required to ile an annual federal partnership return

of income under section 6031(a) of the Internal Revenue Code.

Signed under the penalty of perjury.

Signature of general partner

Date (MM/DD/YY)

Afirmation of Principal Residence

I hereby afirm that I am (we are) the transferor(s) of the property described on this DR 1083 and immediately prior to the

transfer it was my (our) principal residence which could qualify for the exclusion of gain provision of section 121 of the Internal Revenue Code.

Signed under the penalty of perjury.

Signature of transferor

Date (MM/DD/YY)

Spouse's signature if applicable

Date (MM/DD/YY)

Afirmation of No Reasonably Estimated Tax to be Due

I hereby afirm that I am (we are) the transferor(s) or an oficer of the

the transfer.

Please understand before you sign this afirmation that nonresidents of Colorado are subject to Colorado tax on gains from the sale of Colorado real estate to the extent such gains are included in federal taxable income.

Signed under the penalty of perjury.

Signature of transferor, oficer or iduciary

Date (MM/DD/YY)

Spouse's signature if applicable

Date (MM/DD/YY)

Instructions for DR 1083

In general. With certain exceptions, sales of Colorado real property valued of $100,000 of more, and are made by nonresidents of Colorado, are subject to a withholding tax in anticipation of the Colorado income tax that will be due on the gain from the sale.

A transferor who is an individual, estate, or trust will be subject to the withholding tax if either the federal Form

disbursement of the funds resulting from the transaction shows a

A corporate transferor will be subject to the withholding tax if immediately after the transfer of the title to the Colorado real property interest, it has no permanent place of business in Colorado. A corporation will be deemed to have a permanent place of business in Colorado if it is a

Colorado domestic corporation, if it is qualiied by law to

transact business in Colorado, or if it maintains and staffs a permanent ofice in Colorado.

Amount of withholding. The withholding shall be made by the title insurance company or its authorized agent

or any attorney, bank, savings and loan association,

savings bank, corporation, partnership, association, joint stock company, trust, unincorporated organization or any

combination thereof acting separately or in concert that provides closing and settlement services. The amount to be withheld shall be the lesser of: (a) two percent of the selling price of the property interest or, (b) the net proceeds that would otherwise be due to the transferor as shown on the settlement statement.

"Closing and settlement services" means providing services for the beneit of all necessary parties in

connection with the sale, leasing, encumbering, mortgaging, creating a secured interest in and to the real property, and the receipt and disbursement of money in connection with any sale, lease, encumbrance, mortgage, or deed of trust.

Exceptions to Withholding. Withholding shall not be made when:

the selling price of the property is not more than $100,000;

or

the transferor is an individual, estate, or trust and both the Form

disbursement of funds show a Colorado address for the transferor;

or

the transferee is a bank or corporate beneiciary under a mortgage or beneiciary under deed of trust,

and the Colorado real property is acquired in judicial nonjudicial foreclosure or by deed in lieu of foreclosure;

or

the transferor is a corporation incorporated under Colorado law or currently registered with the

the transferor is a corporation incorporated under Colorado law or currently registered with the

Secretary of State's Ofice as authorized to transact

business in Colorado;

or

the title insurance company or the person providing

the closing and settlement services, in good faith, relies upon a written afirmation executed by the

transferor, certifying under the penalty of perjury one of the following:

that the transferor, if a corporation, has a permanent place of business in Colorado;

that the transferor is a partnership as deined

in section 761(a) of the Internal Revenue

Code required to ile an annual federal return

of income under section 6031(a) of the Internal Revenue Code;

that the Colorado real property being conveyed is the principal residence of the transferor which could qualify for the exclusion of gain provisions of section 121 of the Internal Revenue Code;

that the transferor will not owe Colorado income tax reasonably estimated to be due

from the inclusion of the actual gain required to be recognized on the transaction in the gross

income of the transferor.

Normally Colorado tax will be due on any transaction upon which gain will be recognized for federal income tax purposes. Gain will normally be recognized for federal income tax

purposes any time the selling price of the property exceeds the total of the taxpayer's adjusted basis in the property, plus the expenses incurred in the sale of the property. The taxpayer's adjusted basis of the property will normally be the taxpayer's total investment in the property, minus any depreciation thereon he has previously claimed for federal income tax purposes.

Partnership as Transferor. Sales of real property interests by organizations recognized as partnerships for federal income tax purposes and required to ile annual federal

partnership returns of income will not be subject to the

Colorado withholding tax. This exception will not apply to joint ownerships of property which are not recognized as

partnerships for federal income tax purposes. The sale of property jointly owned by a husband and wife, for example, is a sale by two individuals, not a sale by a partnership, and not exempt from withholding tax.

Completion of DR 1083. DR 1083 must be completed and submitted to the Department of Revenue with respect to sales of Colorado real property if Colorado tax was withheld

from the net proceeds from the sale, or if Colorado tax would have been withheld but for the signing of an afirmation by

the transferor.

Information. Forms and additional information are available through the Tax Information Index at WWW.TAXCOLORADO.COM or call (303)

Line 1. Enter the name and address of the transferor.

In the case of multiple transferors of the same real property, a separate DR 1083 must be iled

for each transferor except that if the transferors are husband and wife at the time of closing who held the property as joint tenants, tenants by the entirety, tenants in common, or as community property, and they are both subject to withholding or both exempt from withholding, treat them as a single transferor and list both of their names on line 1. Do not list husband and wife as one transferor if they do not choose to be listed as one transferor. Use the same address as is used

on the federal FORM

available.

Line 3. If both husband and wife are listed on line 1, show both Social Security Numbers on line 3.

Line 5. Type of property sold would be residential, rental, commercial, unimproved land, farm, etc.

Line 6. Address or legal description would be the same as shown on federal FORM

Line 7. Date of closing would be the same as shown on Form

Line 8. Selling price of the property is the contract sales price. Selling price means the sum of:

•the cash paid or to be paid but not including interest;

•the fair market value of other property transferred or to be transferred; and

•the outstanding amount of any liability assumed by the transferee to which the Colorado real property interest is subject immediately before and after the transfer.

Line 9. Selling price of the transferor's interest is that part of the selling price entered on line 8 apportioned to the ownership interest of the transferor for whom the DR 1083 is being prepared. For example, if the property was owned 60% by Smith and 40% by Jones and the property was sold for $150,000, theDR1083beingpreparedforJoneswouldshow $150,000online8and$60,000online9.Notethat it is the amount on line 8 that determines whether or not the $100,000 withholding tax threshold is met, not the amount entered on line 9, but the withholding is to be computed on the amount on line 9 if it is smaller than the amount on line 8.

Line 10 If Colorado tax is withheld on the transaction, check the box on line 10 and show the amount withheld on line 11.

Line 11 If Colorado tax is being withheld on the transfer, thetitleinsurancecompanyorthepersonproviding theclosingandsettlementservicesmustcomplete DR 1079 which is the form used to transmit the tax withheld to the Colorado Department of Revenue.

Line 12. If Colorado tax is not withheld on the transaction, check appropriate box on line 12.

Due date and penalty. The title insurance company or other

person providing the closing and settlement services must ile DR 1083, together with DR 1079 if Colorado tax was

withheld on the transfer, with the Colorado Department of Revenue within 30 days of the closing date of the transaction.

Any title insurance company or its authorized agent which is required to withhold any amount pursuant to

property interests) and fails to do so shall be liable for the greater of ive hundred dollars or ten percent of the amount required to be withheld, not to exceed

dollars.

| Fact | Detail |

|---|---|

| Form Number | DR 1083 |

| Issue Date | 10/17/13 |

| Relevant Department | Colorado Department of Revenue |

| Form Title | Information with Respect to a Conveyance of a Colorado Real Property Interest |

| Primary Purpose | To report information about the conveyance of real property interests in Colorado valued at $100,000 or more by nonresidents |

| Governing Law | §39-22-604.5, C.R.S. (Colorado Revised Statutes) |

| Key Feature | Subject to withholding tax in anticipation of Colorado income tax due on gain from the sale |

| Exception Criteria | No withholding required for properties sold at less than $100,000, among other specified conditions |

Filling out the DR 1083 form is essential for completing the conveyance of a Colorado real property interest, particularly when certain conditions apply that necessitate its submission to the Colorado Department of Revenue. This task, while it may appear daunting at first, can be tackled easily with a step-by-step approach. Here's how to do it:

Once all fields on the DR 1083 form are completed, review the filled-out form to ensure accuracy and completeness. This step is critical in avoiding delays or issues with the conveyance of the real property interest. Ensuring that every detail, from names and addresses to the right checkboxes, is correctly captured will pave the way for a smooth transaction and compliance with Colorado's tax requirements.

What is the purpose of the DR 1083 Colorado form?

The DR 1083 form, titled "Information with Respect to a Conveyance of a Colorado Real Property Interest," serves a critical role in the real estate process in Colorado. Its primary purpose is to provide the Colorado Department of Revenue with important details regarding the transfer of a real property interest within the state. Specifically, the form is used in transactions that might involve the withholding of Colorado income tax from the sale proceeds if the seller is a nonresident of Colorado. By collecting information about the transferor, the property, and the transaction details, this form helps ensure that the appropriate tax obligations are met.

Who needs to file the DR 1083 form?

The DR 1083 form must be filled out and submitted by the party transferring a Colorado real property interest – known as the transferor – under certain circumstances. These circumstances typically involve the sale of real property valued at $100,000 or more by nonresidents of Colorado. Both individuals and entities, such as estates, corporations, trusts, or partnerships that sell or convey real property in Colorado, might be required to complete this form, particularly when Colorado income tax withholding from the sale proceeds is applicable. It ensures compliance with the state’s tax laws regarding the sale of real estate by nonresidents.

What are the exceptions to withholding requirements as indicated on the DR 1083 form?

There are several exceptions to the withholding requirements on the sale of Colorado real property as noted in the DR 1083 form instructions. Withholding is not required if the selling price of the property is not more than $100,000, or if the transferor is a Colorado resident, as evidenced by the addresses on the Form 1099-S and the authorization for disbursement of funds. Other exceptions include transferors who are corporations with a permanent business location in Colorado, properties acquired by banks or corporate beneficiaries in foreclosure, and situations where the transferor can affirm under penalty of perjury specific conditions such as the property being a principal residence qualifying for gain exclusion under IRS rules, or no Colorado income tax being due from any gain on the sale.

How soon after the closing date must the DR 1083 be filed?

For transactions where Colorado tax has been withheld, the DR 1083 form, along with the DR 1079 form if applicable, must be filed with the Colorado Department of Revenue within 30 days following the closing date of the property transaction. This timely filing is crucial to comply with state regulations and avoid potential penalties. It ensures that the tax withheld is properly credited and that all necessary information regarding the property transfer is reported to the state's revenue department. Failure to meet this deadline could lead to fines or penalties, making it important for the transferor and other parties involved in the closing process to be diligent about these requirements.

Filling out the DR 1083 form, which pertains to the conveyance of a Colorado real property interest, requires attention to detail to avoid common mistakes. Here's a list of some errors people often make:

Here are additional considerations that don't directly relate to form errors but are important:

Avoiding these mistakes can help in the smooth processing of the DR 1083 form and ensure compliance with Colorado Department of Revenue requirements.

When managing property transactions in Colorado, specifically involving the DR 1083 form for conveyance of a Colorado real property interest, professionals frequently utilize additional forms and documents to ensure compliance and accuracy in the reporting process. These supplementary documents play crucial roles at various stages of property transactions, from affirming residency status to calculating and reporting taxes due.

These documents work in conjunction with the DR 1083 form to provide a complete and compliant record of the property transaction. Each plays a specific role in capturing the necessary information for tax reporting, legal verification, and transactional clarity. Together, they help streamline the process, ensuring all parties meet their obligations and maintain the integrity of the transaction.

The DR 1083 Colorado form, detailing the conveyance of a Colorado real property interest, shares resemblances with other tax-related documents in its purpose and content layout. Two notable documents similar to the DR 1083 form include the IRS Form 1099-S and the Colorado DR 1079 form. Each document serves as a crucial component in real estate transactions, focusing on the financial and tax implications of property transfers.

The IRS Form 1099-S, "Proceeds from Real Estate Transactions," is particularly similar to the DR 1083 form in its objective to report the sale or exchange of real estate. Like the DR 1083, Form 1099-S collects the seller's information, the property's description, and details of the transaction such as the date of closing and selling price. Both forms ensure accurate reporting to tax authorities, aiding sellers in complying with tax obligations related to gains from property sales. The key difference revolves around their jurisdictional use, with the 1099-S being a federal requirement and the DR 1083 specific to Colorado's tax management.

The Colorado DR 1079 form, "Income Tax Withholding on Real Estate Sales," is directly related to the DR 1083 through their combined use in the state's real estate transactions. The DR 1079 form complements the DR 1083 by facilitating the reporting and payment of withheld Colorado income tax due from the sale of Colorado real property by non-residents. It mandates the withholding agent's details, the amount of tax withheld, and the transferor's information, mirroring the data points in the DR 1083. The interconnectedness of these forms streamlines the process, ensuring compliance with Colorado's tax withholding requirements on property sales, and addresses scenarios where withholding is necessary, further highlighted by the DR 1083's instructions for completing and filing in conjunction with the DR 1079.

Filling out the DR 1083 form, a document concerning the conveyance of Colorado real property interests, needs careful attention to ensure accuracy and compliance with the Colorado Department of Revenue's requirements. Here's a comprehensive guide on what you should and shouldn't do when completing this form:

Following these guidelines when completing the DR 1083 form will help ensure that the process is smooth and free from common mistakes. Taking the time to accurately complete and review this document protects all parties involved in the conveyance of Colorado real property interests.

When it comes to understanding legal forms, misinformation can easily spread. The DR 1083 Colorado form, essential for certain real estate transactions within the state, is no exception. Here, we aim to clear up some common misconceptions that have swirled around this document.

It's only for individuals. A common misconception is that the DR 1083 form is solely for individual use. In fact, the form accommodates a variety of transferors, including estates, corporations, trusts, and more. Its versatility ensures a wide range of entities can comply with Colorado's tax requirements during property conveyance.

It applies to all property sales. Not every property sale in Colorado requires the completion of this form. Specifically, the DR 1083 is geared towards sales of real property valued at $100,000 or more by nonresidents of Colorado. It's this particular subset of transactions that triggers the need for the form, alongside certain withholding tax conditions.

No exemptions exist. Contrary to what some might think, there are indeed exemptions to the withholding requirements stipulated by the form. For example, if the selling price is not more than $100,000, or if the transferor, being an individual, estate, or trust, displays a Colorado address on both the Form 1099-S and the disbursement authorization, withholding might not be necessary.

Withholding rate is fixed. The misunderstanding here is that there's a set percentage universally applied to all transactions. In reality, the amount withheld is the lesser of two figures: either two percent of the selling price of the property interest or the net proceeds due to the transferor as outlined on the settlement statement. This provides a more nuanced approach to withholding that can benefit the transferor under certain circumstances.

All corporations are exempt. While it might seem that corporate transferors have an automatic pass, that's not the case. Exemption for corporations hinges on specific criteria, such as having a permanent place of business in Colorado or being incorporated or registered in Colorado to transact business. The absence of these criteria means the corporation could still be subject to withholding.

Partnerships always trigger withholding. On the contrary, sales by organizations recognized as partnerships under federal tax laws and required to file federal partnership income returns are not subject to Colorado withholding tax. This clarification is crucial for partnerships worried about unanticipated tax obligations during property conveyance.

Every transferor needs a separate form. While it might appear cumbersome, the requirement to file a DR 1083 for each transferor has exceptions. Notably, when transferors are spouses who held the property jointly and are both subject to or exempt from withholding, they could be treated as a single transferor on this form, simplifying the process.

Filing deadlines are flexible. The handling of this form, much like with many legal documents, is under strict deadlines. Specifically, the form, along with a DR 1079 if withholding is applied, must be filed within 30 days of the closing date of the transaction. Believing deadlines are merely suggestive can lead to penalties, emphasizing the importance of timely compliance.

In summary, navigating the DR 1083 Colorado form can seem daunting, but understanding its actual requirements and exemptions helps streamline the process. Armed with the correct information, individuals and entities can confidently manage their obligations when transferring Colorado real property.

Filling out and using the DR 1083 form is an essential step for certain real estate transactions in Colorado, especially for nonresidents. Here are five key takeaways to ensure the process is handled correctly:

In summary, the DR 1083 form is a critical document for real estate transactions involving out-of-state sellers in Colorado. It ensures that income tax due from the gain on the sale of real property is properly collected. Stakeholders involved in such transactions must be aware of the requirements, exceptions, and penalties to ensure a smooth, compliant transfer process.

Ai Miami International University of Art and Design - Simplified process for requesting official transcripts from The Art Institute of Colorado, noting the financial and procedural requirements.

Transfer Car Title Colorado - Whether you're buying, selling, or transferring vehicle ownership, the DR 2395 form is your go-to for official documentation in Colorado.