Fill a Valid Colorado Dr 1191 Form

Fill a Valid Colorado Dr 1191 Form

When it comes to navigating the intricacies of purchasing machinery and machine tools in Colorado, the DR 1191 form serves as a highly important document for both sellers and purchasers. This form, issued by the Colorado Department of Revenue, outlines the qualifications for a sales tax exemption specific to machinery and machine tools that will be used in manufacturing processes. To be eligible, the machinery must not only be used in Colorado but also predominantly for manufacturing tangible personal property intended for sale or profit. This criterion mirrors the eligibility requirements for the federal investment tax credit, limiting the exemption to tangible personal property with a useful lifespan of at least one year and capping qualifying purchases of used equipment at $150,000 annually. Additionally, the machinery or tools must be itemized on a purchase order or invoice that totals more than $500 and must be capitalized as an asset. An important extension of this exemption applies to businesses operating within designated enterprise zones, where additional purchases may also be exempt from state sales and use taxes, underlining the form's significant role in facilitating the growth and operational efficiency of manufacturing enterprises within Colorado. The process of claiming this exemption requires careful adherence to the guidelines set forth on the form, including furnishing a completed copy to the seller and the Department of Revenue while retaining a copy for record-keeping purposes. This ensures that both the selling and purchasing parties are relieved of sales tax liability, positioning the DR 1191 form as a pivotal financial tool for eligible manufacturing entities.

DR 1191 (12/02)

COLORADO DEPARTMENT OF REVENUE

TAXPAYER SERVICE

1375 SHERMAN ST. DENVER, CO 80261 (303)

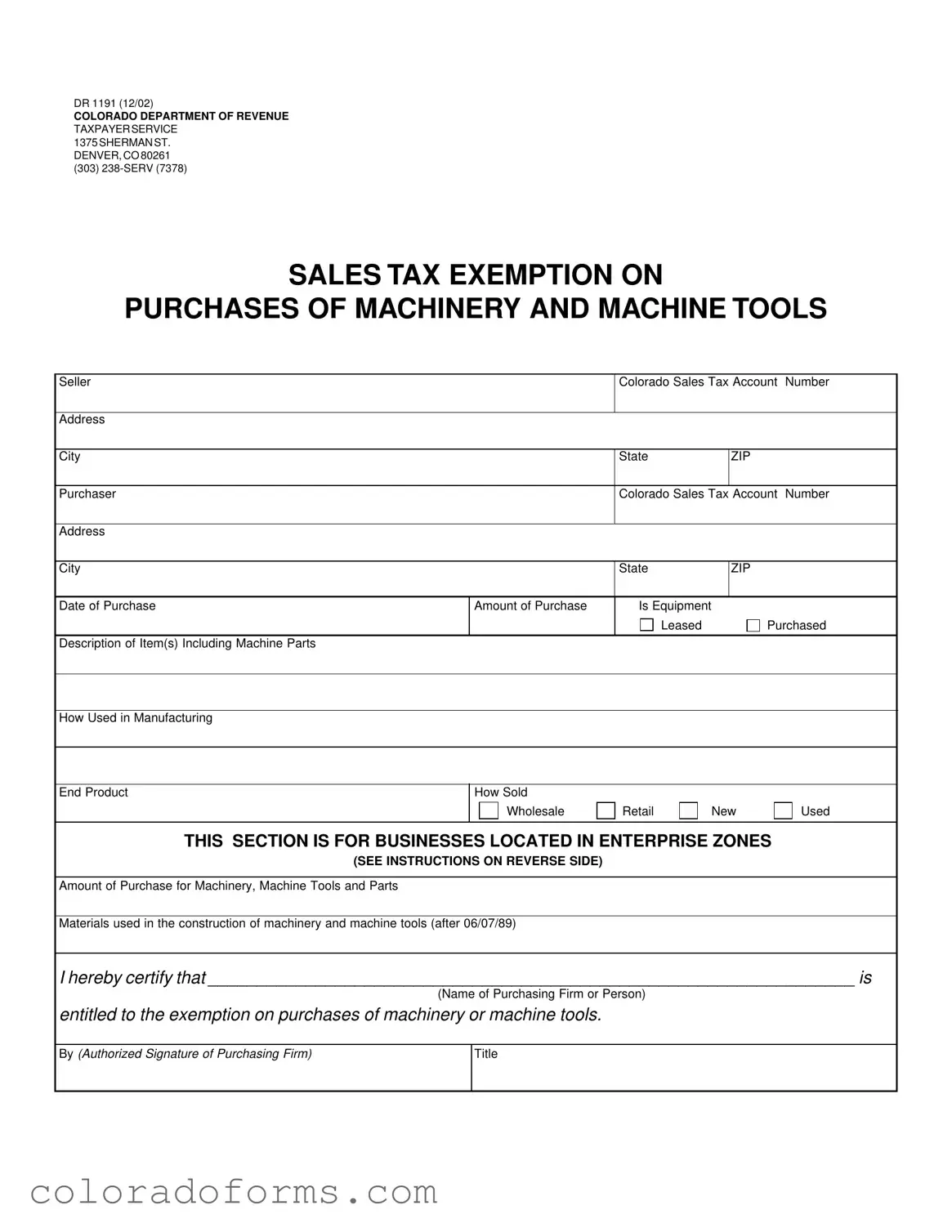

SALES TAX EXEMPTION ON

PURCHASES OF MACHINERY AND MACHINE TOOLS

Seller |

|

|

|

|

Colorado Sales Tax Account |

Number |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Purchaser |

|

|

|

|

Colorado Sales Tax Account |

Number |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Date of Purchase |

Amount of Purchase |

Is Equipment |

|

|

|

|

|

|||||

|

|

|

|

|

Leased |

|

Purchased |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Description of Item(s) Including Machine Parts |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

How Used in Manufacturing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

End Product |

How Sold |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Wholesale |

|

Retail |

|

|

New |

|

|

Used |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

THIS SECTION IS FOR BUSINESSES LOCATED IN ENTERPRISE ZONES

(SEE INSTRUCTIONS ON REVERSE SIDE)

Amount of Purchase for Machinery, Machine Tools and Parts

Materials used in the construction of machinery and machine tools (after 06/07/89)

I hereby certify that __________________________________________________________________ is

|

(Name of Purchasing Firm or Person) |

|

entitled to the exemption on purchases of machinery or machine tools. |

||

|

|

|

By (Authorized Signature of Purchasing Firm) |

|

Title |

|

|

|

DR 1191 INSTRUCTIONS

GENERAL INFORMATION

Purchases of machinery or machine tools and parts thereof are exempt from state sales and use tax when the machinery will be used in manufacturing. [C.R.S.

To qualify the machinery must:

•Be used in Colorado,

•Be used directly and predominantly to manufacture tangible personal property for sale or profit.

•Be of a nature that would have qualified for the federal investment tax credit under the definition of section 38 property found in the Internal Revenue Code of 1954, as amended. This includes tangible personal property with a useful life of one year or more and limits qualifying purchases of used equipment to a maximum of $150,000 annually,

•Be included on a purchase order or invoice totaling more than $500,

•Be capitalized.

ENTERPRISE ZONES

The manufacturing exemption is expanded to exempt additional purchases from sales and use tax when machinery is used solely and exclusively in an enterprise zone. Equipment that is used both within and outside an enterprise zone only qualifies for the regular statewide exemption, as is equipment used at a location prior to that location’s designation as an enterprise zone. [C.R.S.

•Machinery used solely and exclusively in a designated enterprise zone may be capitalized or expensed to qualify for the exemption.

•Materials for construction or repair of machinery or machine tools are exempt from the state sales and use tax if the machinery is used exclusively in an enterprise zone.

•Mining operations are included in the definition of manufacturing when performed in an enterprise zone. For further information, see FYI Sales 69, “Enterprise Zone Exemption for Machinery and Machine Tools Used in Mining.”

LOCAL TAXES

Cities, counties and special districts may or may not exempt manufacturing equipment from local sales taxes. Refer to publication DRP1002 for a list of localities that exempt this equipment from local tax. Special districts that impose sales tax on manufacturing equipment cannot impose use tax on the equipment.

CLAIMING THE EXEMPTION

Complete Form DR 1191 Sales Tax Exemption on Purchases of Machinery and Machine Tools. Give one copy of the completed form to the seller of the machinery and a second copy to the Department of Revenue. The purchaser must also keep a copy. An exemption cannot be claimed for sales tax paid in another state which is credited against Colorado sales or use tax. NOTE: Acceptance of this certificate by the seller removes any sales tax liability from the seller and the purchaser is liable for any subsequent sales or use tax liability for the purchase.

For further information regarding the manufacturing exemption, see FYI Sales 10 available on our Website at WWW.TAXCOLORADO.COM, or call (303)

| Fact | Detail |

|---|---|

| Form Name | DR 1191 |

| Department | Colorado Department of Revenue |

| Purpose | Sales Tax Exemption on Purchases of Machinery and Machine Tools |

| Eligibility Criteria | Machinery must be used in Colorado for manufacturing tangible personal property for sale or profit, directly and predominantly. |

| Equipment Criteria | Must qualify under the definition of section 38 property in the Internal Revenue Code of 1954, as amended, with a useful life of one year or more. |

| Purchase Requirements | Must be included on a purchase order or invoice totaling more than $500 and must be capitalized. |

| Enterprise Zones Special Conditions | Machinery used solely in an enterprise zone may be capitalized or expensed. Materials for construction or repair of such machinery are exempt from state sales and use tax. |

| Governing Law for General Exemption | C.R.S. 39-26-114(11) |

| Governing Law for Enterprise Zones | C.R.S. 39-30-106(1) |

After completing the Colorado DR 1191 form, your next step is to know precisely what to do with it to ensure your purchase qualifies for the sales tax exemption on eligible machinery and machine tools. There are specific steps to properly fill out this form. Following these steps helps make sure that both the seller and purchaser comply with Colorado tax laws and benefit from the state's tax exemption for manufacturing equipment.

Make sure to review the form for accuracy before submitting it. One copy should be given to the seller of the machinery, a second copy must be sent to the Department of Revenue, and it’s important to retain a copy for your records. This form is crucial for ensuring that your purchases are correctly exempted from sales tax, in accordance with Colorado State law.

What is the Colorado DR 1191 form used for?

The Colorado DR 1191 form is specifically designed for businesses to claim sales tax exemption on purchases of machinery and machine tools that are intended for use in manufacturing. This exemption applies to both state sales and use taxes when the machinery or tools will be directly and predominantly used to manufacture tangible personal property for sale or profit.

Who qualifies for the exemption provided by the DR 1191 form?

Any business that purchases machinery or machine tools to be used primarily in manufacturing tangible personal property for sale or profit in Colorado can qualify. However, the equipment must have a useful life of one year or more, and the purchases must be capitalized. Additionally, there's a limit for qualifying purchases of used equipment up to $150,000 annually.

Are there any special conditions for businesses located in Enterprise Zones?

Yes, businesses situated within designated Enterprise Zones in Colorado can benefit from an expanded exemption. This includes the purchase of machinery used solely within an enterprise zone, materials for construction or repair of machinery, and machine tools used exclusively in these zones. Noteworthy, mining operations in an enterprise zone also fit the definition of manufacturing for this exemption.

How does one claim the sales tax exemption using the DR 1191 form?

To claim the exemption, a business must complete the DR 1191 form and distribute copies appropriately: one goes to the seller of the machinery, another to the Department of Revenue, and the purchaser should keep one for their records. This process ensures both the seller and purchaser adhere to Colorado's tax laws regarding the exemption.

What are the implications for the seller when a DR 1191 form is accepted?

Once a seller accepts a completed DR 1191 form, they are relieved of any sales tax liability for that transaction. The onus then shifts to the purchaser to ensure compliance with Colorado sales or use tax laws, including any future liabilities that may arise from the purchase.

Can a business claim an exemption for equipment used outside of Colorado or in mixed-use scenarios?

No, to qualify for the exemption, the machinery must be used in Colorado and directly and predominantly in the manufacturing of tangible personal property intended for sale or profit. Equipment used outside of Colorado or for purposes other than manufacturing does not qualify. However, there is a partial exception for equipment used in an enterprise zone but also outside; it may still qualify for the statewide exemption but not the expanded enterprise zone exemption.

Does the exemption apply to local sales taxes?

This exemption specifically applies to state sales and use taxes. However, local jurisdictions in Colorado have the discretion to exempt or impose their sales taxes on manufacturing equipment. It's essential to consult publication DRP1002 or the local tax authority for guidance on local tax policies concerning manufacturing equipment.

What happens if the machinery is leased rather than purchased?

The DR 1191 form also covers leased machinery and machine tools as long as they are used in manufacturing tangible personal property for sale or profit. The exemption's conditions remain the same, including the requirement for the machinery to be used predominantly and directly in manufacturing processes within Colorado.

Where can additional information about the manufacturing exemption be found?

For more detailed information regarding the manufacturing exemption and the DR 1191 form, businesses can refer to the Colorado Department of Revenue's website at WWW.TAXCOLORADO.COM or contact their Taxpayer Service at (303) 238-SERV (7378). Additionally, FYI Sales 10 and FYI Sales 69 provide further guidance on the enterprise zone exemption and other specifics.

Filling out the Colorado DR 1191 form, which is essential for claiming a sales tax exemption on purchases of machinery and machine tools, often appears straightforward. However, even small mistakes can lead to the denial of an exemption claim. Here is an exploration of common errors to avoid:

Incorrect or Incomplete Seller and Purchaser Information: One of the most frequent mistakes is not filling in the complete details of the seller and purchaser, including the full names, addresses, and Colorado Sales Tax Account Numbers. This information is crucial for the form's validity.

Overlooking the Equipment Lease Section: It's easy to skip the section regarding whether the equipment is leased or purchased. This distinction is significant for tax exemption eligibility, yet it's often overlooked or inaccurately filled.

Failure to Describe the Machinery's Use Thoroughly: Just listing the name or basic function of the machinery isn't enough. It's important to describe how the machinery is used in manufacturing the end product, including any processes it contributes to. This detail helps justify the tax exemption claim.

Inaccurate Classification of Machinery for Enterprise Zones: For businesses located in enterprise zones, machinery usage is subject to additional exemptions. Misclassifying machinery as used exclusively in an enterprise zone when it also functions outside can lead to claim denial. Providing precise information about where and how the machinery is used is essential.

Failing to Retain Copies of the Form: After completing and distributing the form's copies, some forget to keep a copy for their records. However, maintaining a copy is vital for addressing any future disputes or audits regarding the tax exemption status.

To ensure success when applying for this valuable exemption, attention to detail is key. Thoughtfully addressing each section of the DR 1191 form will help streamline the approval process, allowing businesses to benefit from significant savings on essential machinery and equipment.

When dealing with the Colorado DR 1191 form, which exempts purchases of machinery and machine tools from state sales and use tax for manufacturing, you often need additional documentation to ensure compliance and accuracy in your filing. These documents support various aspects of the exemption claim, from proving the eligibility of the business to detailing the use of the purchased equipment.

Together, these documents and forms provide a comprehensive framework for businesses to accurately apply for and substantiate their eligibility for the Colorado DR 1191 sales tax exemption. Keeping thorough and organized records of these items not only facilitates the exemption process but also ensures businesses remain compliant with Colorado tax laws.

The Colorado DR 1191 form is similar to a number of other documents that facilitate tax exemptions for specific purchases under various conditions. Primarily, this form grants businesses a sales tax exemption on purchases of machinery and machine tools when these items are used directly in manufacturing processes. The uniqueness of the DR 1191 form is attributed to its focus on manufacturing equipment used within Colorado, especially highlighting its applicability to businesses operating within enterprise zones.

Firstly, one can liken the DR 1191 to the Federal Form 4562, which is used for Depreciation and Amortization. Just like the DR 1191, Form 4562 is filled out by businesses to report the depreciation of property or equipment over a specific period — a crucial step for tax deduction purposes related to capital expenditures. However, while Form 4562 applies to a broader scope of property across any location within the United States, the DR 1191 zooms in on machinery and machine tools used in the manufacturing sector within Colorado, offering a sales tax exemption rather than a depreciation schedule.

Similarly, the form bears resemblance to State Specific Sales Tax Exemption Certificates used throughout the United States. Most states offer forms that allow businesses to purchase goods without paying state sales tax if those goods are to be either resold as part of other products or used in the production process. The similarity here lies in the purpose: both sets of forms are designed to promote commercial activities by reducing the upfront costs associated with purchasing equipment or inventory. The difference, however, revolves around the specific qualifications for exemptions and the types of eligible goods. Colorado’s DR 1191 specifically targets machinery and machine tools used in manufacturing and has particular provisions for equipment used in enterprise zones.

Lastly, the DR 1191 has parallels with the Manufacturing and Research & Development Equipment Exemption Certificate forms found in states like California. These exemptions are designed to support manufacturing and R&D activities within the state by providing tax relief on the purchase of equipment and machinery. While both this exemption and Colorado's DR 1191 aim to bolster economic activities related to manufacturing, the criteria, and scope of qualified machinery, and the process of claiming the exemption can vary significantly from state to state. In Colorado, the emphasis on enterprise zones and specific eligibility criteria outlined in DR 1191 highlights a tailored approach to encouraging investments in the manufacturing sector within its geopolitical boundaries.

When filling out the Colorado DR 1191 form for sales tax exemption on purchases of machinery and machine tools, there are critical dos and don'ts to keep in mind. Following these guidelines will help ensure that your submission is successful and compliant with Colorado's Department of Revenue requirements.

Do:By adhering to these guidelines, businesses can smoothly navigate the exemption process, ensuring that they correctly benefit from Colorado’s sales tax exemption on eligible machinery and machine tool purchases.

When discussing the Colorado DR 1191 form, several misconceptions come up frequently. Let's clear up these misunderstandings to ensure you're on the right track.

Only newly purchased machinery qualifies for the exemption: It's a common belief that the sales tax exemption on the DR 1191 form only applies to brand-new machinery. However, the exemption also extends to used machinery, as long as the purchase meets the specific criteria outlined in the form, like being used directly and predominantly to manufacture tangible personal property for sale or profit, and having a useful life of more than one year.

The exemption automatically applies to all business purchases: Some people think that as long as they're running a business, all their purchases of machinery would qualify for a sales tax exemption. In reality, to qualify, the machinery must be used in Colorado and directly in the manufacturing of tangible personal property meant for sale or profit. Additionally, certain spending caps and requirements must be met.

Any kind of machinery can qualify: Not all machinery will qualify for the exemption. The equipment must have a role in manufacturing tangible personal property for sale or profit and should align with the federal investment tax criteria. Also, the total on a purchase order or invoice must exceed $500, and the item must be capitalized on the business' books.

There's no limit to how much you can spend: Although the DR 1191 form facilitates a sales tax exemption for qualifying purchases, there's an annual cap on qualifying purchases of used equipment, set at $150,000. This is a detail businesses must pay attention to when planning their equipment investments.

Only businesses in enterprise zones benefit: While it's true that the manufacturing exemption is expanded for businesses operating solely in enterprise zones, allowing for both capitalized and expensed machinery to qualify, the basic exemption still applies statewide. The additional benefits for enterprise zones include exemptions for materials used in machinery construction or repair, underlining the broader applicability of this exemption.

Completing and submitting the DR 1191 form is optional: Some may think that if they meet all the requirements, the exemption applies automatically. However, to actually receive the exemption, the form must be properly completed and submitted, with a copy given to the seller, one to the Department of Revenue, and one retained by the purchaser. Neglecting to complete this step places the purchaser at risk for later sales or use tax liability.

Understanding these misconceptions can save you time and ensure you fully benefit from the sales tax exemption offered by Colorado for machinery and machine tools purchases under certain conditions. Always remember to consult with a tax professional or the Department of Revenue to ensure your purchases comply.

The Colorado DR 1191 form is a critical document for businesses aiming to leverage the state sales and use tax exemption on machinery and machine tools purchases. Understanding the nuances of this form can unlock significant savings, particularly for manufacturing entities. Here are five key takeaways about filling out and using the Colorado DR 1191 form:

Armed with the correct understanding of the DR 1191 form, businesses in Colorado can efficiently navigate the process of claiming exemptions on purchases of machinery and machine tools. This not only aids in compliance with state tax laws but also optimizes capital expenditure, especially for entities involved in manufacturing.

Dr2173 Motor Vehicle Bill of Sale Form - Completion of the DR 2424 form is a critical step in acquiring a legal title for vehicles rebuilt from salvage in Colorado.

Free Will Template Colorado - This form is a key tool in avoiding the intestacy process in Colorado, which can lead to unintended consequences for asset distribution.

Colorado Ucc3 - Includes optional contact information for a person to reach out to with questions about the filing.