Fill a Valid Colorado Dr 0204 Form

Fill a Valid Colorado Dr 0204 Form

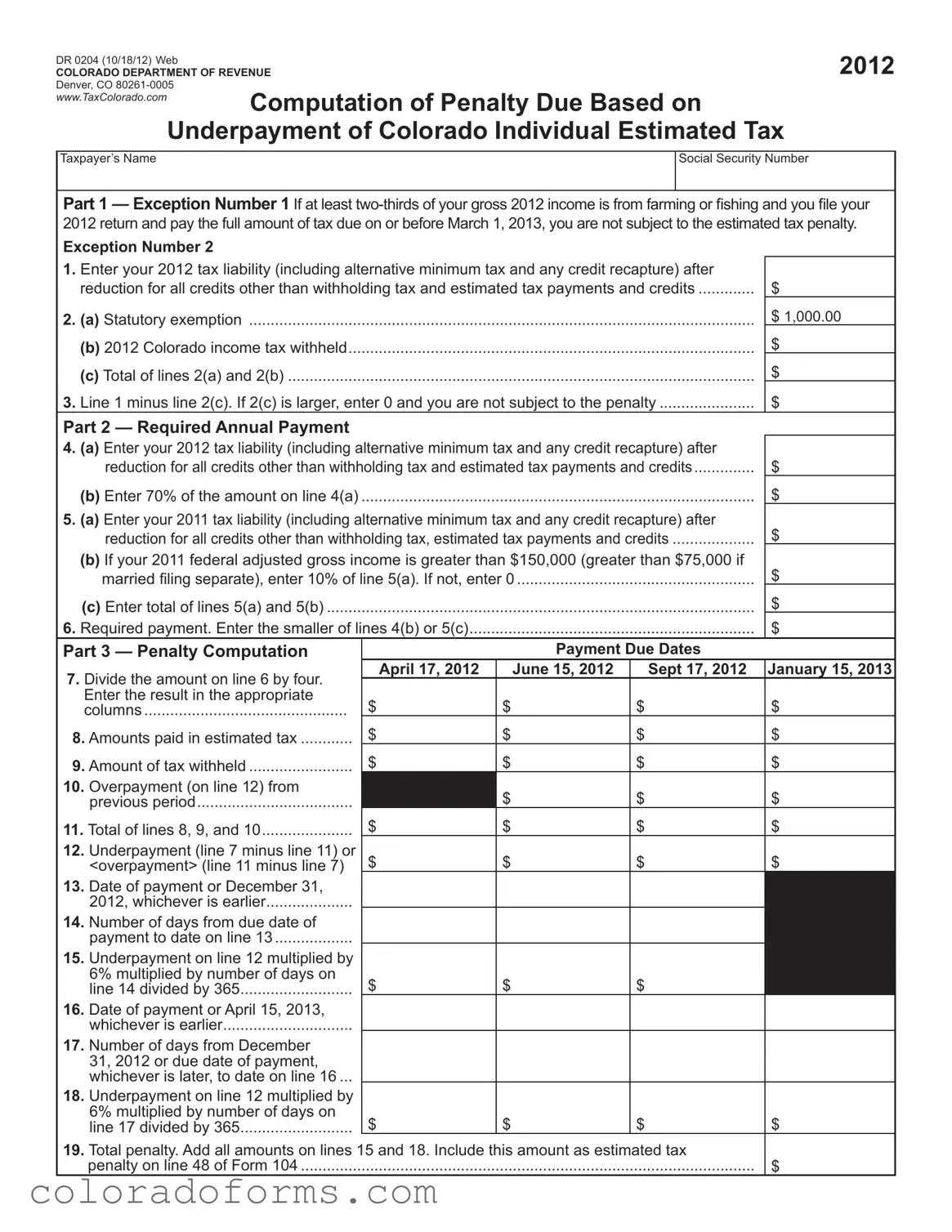

The Colorado DR 0204 form, issued by the Colorado Department of Revenue as of October 18, 2012, plays a crucial role in the financial obligations of individuals who owe estimated taxes. This form is designed to assist taxpayers in calculating any penalties due on underpayments of Colorado individual estimated tax. Detailed within the document are precise criteria to determine whether a taxpayer is subject to these penalties, including specific exceptions for certain income types and timely payment conditions. These exceptions provide relief for individuals with significant portions of their income derived from farming or fishing, given certain deadlines are met. Beyond identifying eligibility for penalty assessment, the DR 0204 form outlines a methodical process for calculating the required annual payment, comparing 70% of the current year's net tax liability against 100% or 110% of the previous year's liability, with adjustments based on federal adjusted gross income. The form further guides the taxpayer through the computation of any penalties due, factoring in payment due dates, amounts already paid, and any overpayments from previous periods. For those whose income varies throughout the year, the form offers an annualized installment method schedule, allowing a tailored approach to estimated tax payments. Complete with instructions and examples, the DR 0204 form is a comprehensive tool for navigating the complexities of estimated tax payments and penalties, ensuring taxpayers meet their obligations and minimize potential penalties.

DR 0204 (10/18/12) Web |

2012 |

COLORADO DEPARTMENT OF REVENUE |

Denver, CO |

|

WWW.TAXCOLORADO.COM |

Computation of Penalty Due Based on |

|

|

|

Underpayment of Colorado Individual Estimated Tax |

Taxpayer’s Name

Social Security Number

Part 1 — Exception Number 1 If at least

Exception Number 2

1.Enter your 2012 tax liability (including alternative minimum tax and any credit recapture) after reduction for all credits other than withholding tax and estimated tax payments and credits .............

2.(a) Statutory exemption .....................................................................................................................

(b)2012 Colorado income tax withheld..............................................................................................

(c)Total of lines 2(a) and 2(b) ............................................................................................................

3.Line 1 minus line 2(c). If 2(c) is larger, enter 0 and you are not subject to the penalty ......................

$

$1,000.00

$

$

$

Part 2 — Required Annual Payment

4.(a) Enter your 2012 tax liability (including alternative minimum tax and any credit recapture) after reduction for all credits other than withholding tax and estimated tax payments and credits..............

(b)Enter 70% of the amount on line 4(a) ...........................................................................................

5.(a) Enter your 2011 tax liability (including alternative minimum tax and any credit recapture) after reduction for all credits other than withholding tax, estimated tax payments and credits ...................

(b)If your 2011 federal adjusted gross income is greater than $150,000 (greater than $75,000 if married iling separate), enter 10% of line 5(a). If not, enter 0 .......................................................

(c)Enter total of lines 5(a) and 5(b) ...................................................................................................

6.Required payment. Enter the smaller of lines 4(b) or 5(c)..................................................................

$

$

$

$

$

$

Part 3 — Penalty Computation |

|

Payment Due Dates |

|

||

7. Divide the amount on line 6 by four. |

April 17, 2012 |

June 15, 2012 |

Sept 17, 2012 |

January 15, 2013 |

|

|

|

|

|

||

Enter the result in the appropriate |

$ |

$ |

$ |

$ |

|

columns |

|||||

8. |

Amounts paid in estimated tax |

$ |

$ |

$ |

$ |

9. |

Amount of tax withheld |

$ |

$ |

$ |

$ |

10.Overpayment (on line 12) from

previous period |

|

$ |

$ |

$ |

11. Total of lines 8, 9, and 10 |

$ |

$ |

$ |

$ |

12.Underpayment (line 7 minus line 11) or

<overpayment> (line 11 minus line 7) |

$ |

$ |

$ |

$ |

13.Date of payment or December 31, 2012, whichever is earlier....................

14.Number of days from due date of payment to date on line 13..................

15.Underpayment on line 12 multiplied by 6% multiplied by number of days on

line 14 divided by 365 |

$ |

$ |

$ |

16.Date of payment or April 15, 2013, whichever is earlier..............................

17.Number of days from December 31, 2012 or due date of payment, whichever is later, to date on line 16 ...

18.Underpayment on line 12 multiplied by 6% multiplied by number of days on

line 17 divided by 365 |

$ |

$ |

$ |

$ |

19.Total penalty. Add all amounts on lines 15 and 18. Include this amount as estimated tax

penalty on line 48 of Form 104 |

$ |

Part 4 — Annualized Installment Method Schedule

20. Ending date of annualization period |

March 31, 2012 |

May 31, 2012 |

August 31, 2012 |

Dec 31,2012 |

21. Colorado taxable income computed |

$ |

$ |

$ |

$ |

through the date on line 20 |

||||

22. Annualization factor |

4 |

2.4 |

1.5 |

1 |

|

|

|

|

|

23. Annualized taxable income |

$ |

$ |

$ |

$ |

Line 21 times line 22 |

||||

24. Annualized Colorado tax |

$ |

$ |

$ |

$ |

Line 23 times 4.63% |

||||

25. Applicable percentage |

17.5% |

35% |

52.5% |

70% |

|

|

|

|

|

26. Installment payment due. |

|

|

|

|

Line 24 multiplied by line 25, minus |

|

|

|

|

amounts entered on line 26 in earlier |

|

|

|

|

quarters.Enter here and on line 7 |

$ |

$ |

$ |

$ |

Instructions for DR 0204

Part 1 Generally you are subject to an estimated tax penalty if your 2012 estimated tax payments are not paid in a timely manner. The estimated tax penalty will not be assessed if either of the exceptions are met.

Part 2 The required annual amount to be paid is the lesser of:

1.70% of actual 2012 net Colorado tax liability.

2.100% of preceding year’s net Colorado tax liability.

(This amount only applies if the preceding year was a

3.110% of preceding year’s net Colorado tax liability.

(This amount only applies if the preceding year was a

Colorado return.)

Part 3 If neither exception applies to you, compute your penalty on lines 7 through 19 of Form 204. Complete each column before going on to the next column. See FYI

Income 51, Estimated Income Tax, regarding estimated tax payment allocation on line 8. The amount entered on line 10 is the net overpayment from the preceding period.

On line 17, if the payment was made prior to January 1,

2013, enter “0.” If the tax return is iled and any tax due is paid by January 31, 2013, no penalty will be computed

in column four. Estimated tax payments from a farmer or isherman are due in a single payment by January 17,

2013 and only column four is used to compute the penalty.

Part 4 Taxpayers who do not receive income evenly during the year may elect to use the annualized income installment method to compute their estimated tax payments if they elect annualized installments for the payment of their federal income tax. Complete the annualized installment method schedule to compute the amounts to enter on line

7. See FYI Income 51 regarding this computation method.

Example: Taxpayer's net tax liability for 2012 is $10,000. He had $1,000 withholding and none of the exceptions apply. He paid $4,000 on June 12, 2012, and made no additional estimated tax payments.

|

April 17 |

June 15 |

September 17 |

January 15 |

Line 7 |

$1,750 |

$1,750 |

$1,750 |

$1,750 |

Line 8 |

$0 |

$4,000 |

$0 |

$0 |

Line 9 |

$250 |

$250 |

$250 |

$250 |

Line 10 |

— |

— |

$1,000** |

— |

Line 11 |

$250 |

$4,250 |

$1,250 |

$250 |

Line 12 |

$1,500 |

$(2,500) |

$500 |

$1,500 |

Line 13 |

6/12/12 |

6/12/12 |

12/31/12 |

— |

Line 14 |

56 |

— |

107 |

— |

Line 15 |

$13.81 |

— |

$8.79 |

— |

Line 16 |

6/12/12 |

6/12/12 |

4/15/13 |

4/15/13 |

Line 17 |

0 |

0 |

108 |

91 |

Line 18 |

0 |

0 |

$8.85 |

$22.38 |

Line 19 |

$53.83 |

|

|

|

** June 12 Payment |

|

$4,000 |

April withholding |

|

250 |

June withholding |

|

250 |

|

|

$4,500 |

April installment |

$1,750 |

|

June installment |

1,750 |

3,500 |

Overpayment to September |

$1,000 |

|

For additional information regarding the estimated tax penalty see FYI Income 51, which is available at WWW.TAXCOLORADO.COM

| Fact | Detail |

|---|---|

| Form Number | DR 0204 |

| Revision Date | October 18, 2012 |

| Issuing Authority | Colorado Department of Revenue |

| Purpose | Computation of Penalty Due Based on Underpayment of Colorado Individual Estimated Tax |

| Key Components | Taxpayer's Name, Social Security Number, Computation Sections for Penalty on Underpayment |

| Exceptions to Penalty | Income from farming or fishing (if ⅔ of gross income), tax liabilities met before specific deadlines |

| Required Annual Payment Calculation | Based on the lesser of 70% of actual net Colorado tax liability or 100%/110% of the preceding year’s net Colorado tax liability, dependent on income |

| Penalty Computation | Calculated if estimated tax payments are not paid in a timely manner, with specific calculations and instructions provided in the form |

| Governing Laws | Colorado Revised Statutes and Colorado Department of Revenue regulations pertaining to individual income tax |

| Annualized Installment Method | Available for taxpayers with uneven income through the year, with specific guidelines for computation |

Filling out the Colorado DR 0204 form is a process that ensures proper calculation and reporting of any penalties due on underpayments of estimated tax by individuals. This document may seem daunting initially, but with straightforward step-by-step guidance, taxpayers can navigate through it efficiently. Whether you're self-employed, experiencing uneven income through the year, or have additional sources of income that require you to make estimated tax payments, understanding how to fill this form correctly is vital. Here are the necessary steps laid out to assist you in completing the Colorado DR 0204 form.

After carefully following these steps, review your entries to ensure accuracy before submitting the form. This detailed approach helps prevent mistakes and ensures that you're complying with Colorado's tax regulations regarding estimated tax payments and potential penalties.

What is the Colorado DR 0204 form?

The Colorado DR 0204 form is a document used to calculate penalties related to the underpayment of estimated taxes by individuals. This computation is necessary when individuals have not paid their estimated tax payments for the year on time or in the correct amount. The form is structured to help taxpayers determine if they owe a penalty and, if so, calculate the exact amount owed to the Colorado Department of Revenue.

Who needs to fill out the Colorado DR 0204 form?

Individuals who did not pay their estimated taxes correctly or on time for the tax year need to fill out the DR 0204 form. This typically applies to those who have income not subject to withholding tax, such as earnings from self-employment, interest, dividends, rents, or alimony. It's crucial for taxpayers who anticipate owing $1,000 or more in Colorado tax after subtracting withholdings and credits to review their need for this form.

Are there any exceptions to avoid the penalty calculated on the DR 0204 form?

Yes, there are exceptions that can help an individual avoid the penalty for underpayment of estimated taxes. The first exception is for individuals whose gross income is at least two-thirds from farming or fishing; if they file their return and pay the full tax due by March 1 following the tax year, no penalty is applied. Additionally, if the sum of the taxpayer's withholding tax and estimated tax payments equals or exceeds the amount of tax shown on their return for the previous year, they may not be subject to the penalty.

How is the required annual payment calculated on the form?

The required annual payment amount on the DR 0204 form is the lesser of 70% of the current year's net Colorado tax liability or 100% (or 110% for higher income earners) of the previous year's net Colorado tax liability. This calculation is aimed at ensuring taxpayers pay a sufficient amount of their estimated taxes throughout the year to avoid a penalty.

What are the payment due dates for estimated tax payments?

Estimated tax payments are due in four equal installments on April 15, June 15, September 15 of the tax year, and January 15 of the following year. These dates are critical for avoiding penalties for underpayment, as payments must be made on or before these deadlines.

Can taxpayers use the annualized installment method when calculating the penalty?

Yes, taxpayers who do not receive their income evenly throughout the year have the option to calculate their estimated tax payments using the annualized income installment method. This method takes into account when the income was earned during the year, allowing for potentially smaller penalty calculations due to uneven income distribution. To use this method, taxpayers must complete the annualized installment method schedule on the DR 0204 form.

Where can individuals find more information or assistance with the DR 0204 form?

For more detailed information or assistance with filling out the DR 0204 form, individuals can visit the Colorado Department of Revenue's official website at WWW.TAXCOLORADO.COM. Additionally, the FYI Income 51 publication available on the website provides extensive guidance on estimated tax payments and penalties.

Filling out tax forms can be complicated and sometimes mistakes happen, especially with the Colorado DR 0204 form, which relates to the computation of the penalty due based on the underpayment of Colorado Individual Estimated Tax. Awareness of common mistakes can help ensure the process is smoother and more accurate. Here are eight common mistakes to be aware of when completing this form:

Understanding and avoiding these common mistakes can aid in the accurate completion of the DR 0204 form, ensuring taxpayers meet their obligations correctly and possibly saving them from unnecessary penalties. It's always beneficial to review each section carefully, consult the available guidelines like FYI Income 51, or seek professional assistance when uncertain about the form's requirements.

When handling taxes, especially when considering the Colorado DR 0204 form for the computation of penalty due based on underpayment of Colorado individual estimated tax, it's common for individuals to encounter or need additional forms and documents. This necessity stems from various circumstances such as reporting additional income, adjusting previously filed returns, or making estimated payments. Here’s a pertinent set of documents often required in conjunction with the DR 0204 form:

Understanding these forms and documents and knowing when they're necessary can simplify your tax filing process and help avoid penalties for underpayment or incorrect filing. Each has a specific purpose, addressing various elements of an individual's financial circumstances, from adjusting for credits and deductions to accounting for income from multiple states. If you’re unsure about which forms apply to your situation, consider seeking help from a tax professional. Accurate and timely submission of these forms, including DR 0204, ensures compliance with Colorado tax laws and helps manage your financial obligations effectively.

The Colorado Dr 0204 form is similar to other documents used by both the federal government and various states to ensure that taxpayers adequately pay their estimated taxes throughout the year, thus preventing underpayment penalties. These documents typically feature sections dedicated to calculating the taxpayer's estimated tax liability, determining the necessary quarterly or annual payments, and computing any potential penalties due to underpayment.

Internal Revenue Service (IRS) Form 1040-ES, "Estimated Tax for Individuals," is one such document that closely mirrors the purpose and structure of the Colorado Dr 0204 form. Both forms require taxpayers to project their income, deductions, and credits for the year, calculate their tax liability, and determine the required installment payments to avoid penalties. The IRS form applies to federal taxes, while the Dr 0204 is specific to Colorado state taxes, but the underlying principle of preventing underpayment penalties through estimated quarterly payments is a staple of both documents. Furthermore, both forms provide instructions for adjusting payments if one's income fluctuates throughout the year, incorporating special rules for specific categories of taxpayers, such as farmers or fishermen, who have unique payment schedules.

California Form 540-ES, "Estimated Tax for Individuals," is another document with a similar function. Like the Colorado Dr 0204 form, California's version is designed for state residents to calculate and pay their estimated tax on income not subject to withholding. This might include earnings from self-employment, investments, and other sources. The 540-ES also features a worksheet to assist taxpayers in estimating their income and deductions for the year, calculating their tax, and determining the amount of their estimated tax payments to avoid underpayment penalties. Both the California 540-ES and the Colorado Dr 0204 include provisions to compute penalties if the estimated payments made throughout the year do not meet the required thresholds based on prior year's tax or the current year's expected liability.

Despite the differences in jurisdiction and some specifics of the tax codes, the integral purpose of these forms—to facilitate the advance payment of estimated tax liability and to avert penalties for underpayment—remains consistent. They offer structured guidance to taxpayers, ensuring compliance with tax laws by making periodic payments towards their expected tax obligation based on the income that is not subject to withholding at the source.

Filling out the Colorado DR 0204 form, related to the computation of penalty due based on underpayment of Colorado Individual Estimated Tax, requires attention to detail and understanding of your tax situation. Below are essential dos and don'ts to help ensure accuracy and compliance.

Accurately filling out the DR 0204 form is essential to avoid unnecessary penalties and ensure compliance with Colorado tax laws. Take your time to understand each part of the form and seek clarification from tax professionals or the Department of Revenue resources if necessary.

Navigating tax forms can be daunting, and the Colorado DR 0204 form, which is related to the computation of penalties based on underpayment of Colorado individual estimated tax, is no exception. To bring clarity to this essential piece of tax documentation, let’s debunk ten common misconceptions.

Understanding the nuances of the Colorado DR 0204 form can significantly demystify the process of handling underpayments and penalties on estimated tax. By clarifying these misconceptions, taxpayers can approach their tax obligations with greater confidence and accuracy.

When dealing with the Colorado DR 0204 form, which is focused on the computation of penalties due based on the underpayment of Colorado individual estimated tax, understanding the rules and procedures is crucial. Below are key takeaways for accurately filling out and using this form:

The Colorado DR 0204 form is an essential document for those needing to compute penalties related to underpaid estimated taxes. Careful attention to the form’s requirements and deadlines can help minimize any potential financial penalties.

How Long Do You Have to Live in Colorado to Be a Resident - It is important for vehicle owners to keep a copy of the completed DR 2680 form for their records.

Colorado State Income Tax Form - Timely submission of the DR 8440 form is essential for uninterrupted business operations in the liquor sector.