Fill a Valid Colorado Dr 0106Ep Form

Fill a Valid Colorado Dr 0106Ep Form

Understanding the intricacies of state tax obligations is crucial for nonresident individuals earning income in Colorado. The Colorado Department of Revenue has created a specific form, the DR 0106EP, for the 2014 tax year to facilitate the process of estimating and paying taxes for nonresident composite filers. This form serves as a worksheet and a payment voucher, guiding individuals through calculating their estimated Colorado taxable income, applying the current tax rate of 4.63%, and subtracting any eligible credits to determine the net estimated tax. Essential for ensuring compliance, the form outlines four payment installments with clear due dates throughout the fiscal year, emphasizing the importance of timely submissions to avoid penalties. It includes provisions for utilizing overpayments from the previous year and details the method of payment, including the encouragement of electronic transactions for efficiency and security. The DR 0106EP form simplifies the estimated tax payment process, providing a structured approach for nonresident individuals included in a composite filing to meet their tax obligations. With options for electronic filing and payment, the Colorado Department of Revenue promotes an eco-friendly and convenient way for taxpayers to manage and submit their estimated taxes, ensuring that individuals can easily adhere to Colorado's tax requirements without unnecessary complications.

=DO=NOT=SEND=

DR 0106EP (10/19/22)

COLORADO DEPARTMENT OF REVENUE

Denver CO

Tax.Colorado.gov

Colorado

Instructions

Taxpayers are required to make estimated payments during the tax year if their Colorado income tax due will exceed certain thresholds. This form is used for partnerships and S corporations to make estimated payments.

General Rule

In most cases, a partnership or S corporation must pay estimated tax if it will file a composite return on behalf of nonresident partners, and the Colorado income tax liability for any individual partner or shareholder per the composite return will be more than $1,000 for 2023

A partnership or S corporation that elects to be subject to tax at the entity level under section

Required Payments

In general, payments are required quarterly, and the amount due is 25% of the required annual payment. The required annual payment is generally 70% of the actual net Colorado tax liability for the current year, or 100% of the actual net Colorado tax liability for the preceding year (whichever is less). For more information on calculating estimated payment for nonresident partners and shareholders included in a composite return, please see the Individual Income Tax Guide.

Please see the Corporate Income Tax guide if the partnership or S corporation intends to make an election under the SALT Parity Act.

Calculating the Payment

Estimated tax payments must be made on a quarterly basis.

Payments and forms should be submitted using the same account number as will be used on the Colorado Partnership and S Corporation and Composite Nonresident Income Tax Return (DR 0106). If, for any reason, the account numbers are inconsistent, the Department must be notified in writing prior to filing the DR 0106. Mail this notification to:

Colorado Department of Revenue

Denver, CO

being billed, see form DR 0204, Underpayment of Individual Estimated Tax (composite filers) or form DR 0205, Underpayment of Corporate Estimated Tax (entities making an election under the SALT Parity Act).

Refunds

Estimated tax payments can only be claimed as prepayment credit on the 2023 Colorado income tax return. Therefore, estimated payments cannot be refunded until the 2023 Colorado income tax return is filed.

SALT Parity Act Election

A partnership or S corporation may, on an annual basis, elect to be subject to tax at the entity level under the SALT Parity Act (section

Go Green with Revenue Online

Colorado.gov/RevenueOnline allows taxpayers to file taxes, remit payments and monitor their tax accounts. DR 0106EP is not required to be sent if electronic payment is remitted through this site. Please be advised that a nominal processing fee may apply to electronic payments.

Pay by Electronic Funds Transfer (EFT)

EFT payments can be made safely, for free, and can be scheduled up to 12 months ahead of time to avoid forgetting to make a quarterly payment. This requires

Visit

Additional information, guidance publications and forms are available at Tax.Colorado.gov, or you can call

Penalties

Failure to timely remit estimated tax will result in an estimated tax penalty. An estimated tax penalty will also be calculated for each missed or underpaid payment.

For calculation specifics, or to remit this penalty before

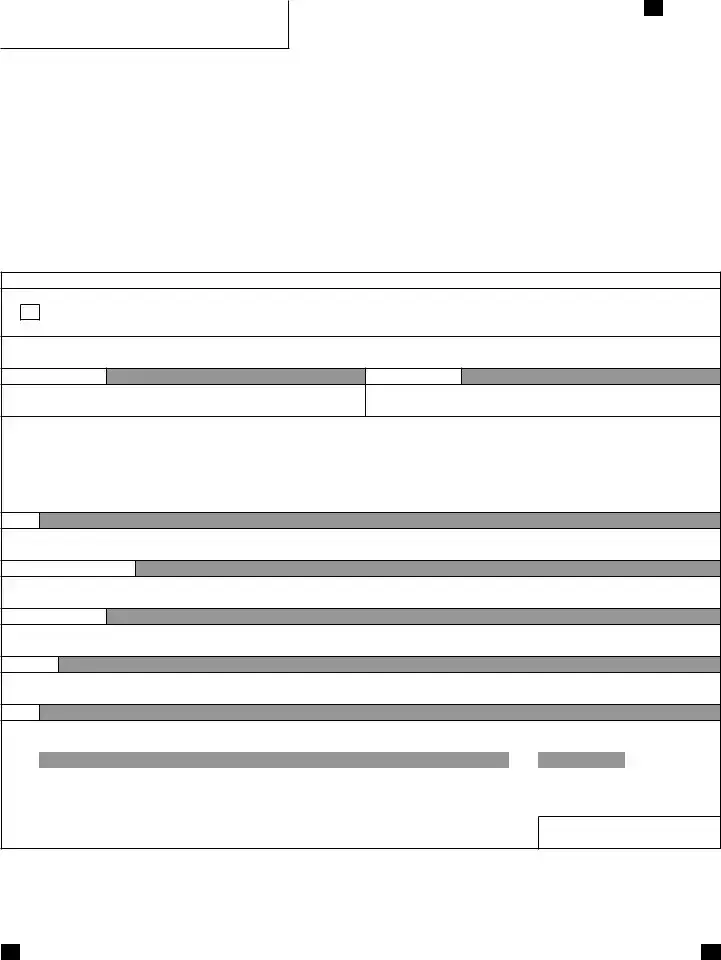

*230106EP19999*

DR 0106EP (10/19/22) |

(0042) |

COLORADO DEPARTMENT OF REVENUE |

Denver CO

Tax.Colorado.gov

Page 1 of 1

2023 Colorado

Payment Form

Only return this payment form with a check or money order.

DO NOT CUT – Return Full Page

DR 0106EP

Mark this box to indicate that this

For the calendar year 2023 or the fiscal year:

Beginning (MM/DD/23)

Ending (MM/DD/YY)

Return the DR 0106EP with check or money order payable to the “Colorado Department of Revenue”. Mail payments to Colorado Department of Revenue, Denver, Colorado

FEIN

Colorado Account Number

Organization Name

Address

City

State |

|

ZIP |

|

Due Date (MM/DD/YY) |

|

|

|

|

|

Amount of Payment

The State may convert your check to a

$

DO NOT CUT – Return Full Page. IF NO PAYMENT IS DUE, DO NOT FILE THIS FORM.

| Fact | Detail |

|---|---|

| Form Number and Title | DR 0106EP - 2014 Colorado Estimated Tax — Composite Nonresident Worksheet |

| Issuing Authority | Colorado Department of Revenue |

| Purpose | To calculate and pay estimated tax for nonresident individuals included in a composite filing for Colorado-source income. |

| Application | Nonresident individuals expected to owe more than $1,000 in Colorado tax after credits must pay estimated tax. |

| Payment Schedule | Quarterly payments due on April 15, June 15, September 15, and January 15 (of the following year). |

| Method of Calculation | 70% of actual net Colorado tax liability or 100%/110% of the preceding year's net Colorado tax liability, based on certain conditions. |

| Electronic Payment Encouragement | Strongly recommends electronic or EFT payments to avoid problems and delays, with resources like www.Colorado.gov/RevenueOnline and EFT pre-registration provided. |

| Governing Laws | Colorado state law, as applicable to nonresident income taxation and estimated tax payments. |

Preparing and submitting the Colorado DR 0106EP form is a key step for nonresident individuals participating in a Colorado composite filing. This process involves calculating and forwarding estimated tax payments based on Colorado-sourced income. To ensure accuracy and compliance, individuals should follow the step-by-step instructions carefully. It's also recommended to make these payments electronically when possible, to streamline the process and avoid any potential errors or delays.

By following these steps, you can accurately complete and submit the DR 0106EP form, thereby fulfilling your estimated tax payment obligations for Colorado. Remember, timely and accurate payments can help avoid penalties. If you have any questions or need further assistance, resources and contact information are available at www.TaxColorado.com.

What is the purpose of the Colorado DR 0106EP form?

The Colorado DR 0106EP form serves as a means for nonresident individuals, included in a composite filing through Form 106, to make estimated tax payments on income earned from Colorado sources. This is necessary when income is not subject to withholding and is aimed at ensuring that the state receives its due taxes on all income generated within Colorado by those who do not reside in the state. The process helps to avoid underpayment of taxes and the potential for facing penalties at the end of the tax year.

Who needs to file the DR 0106EP form?

Nonresident individuals who expect to owe more than $1,000 in Colorado tax for the year, after accounting for any withholding or refundable credits, are required to file the DR 0106EP form. This requirement applies to each individual included in the composite return, ensuring that all appropriate estimated tax payments are made in a timely and accurate manner for income derived from sources within Colorado.

How do I calculate the estimated tax payments using the DR 0106EP worksheet?

To calculate estimated tax payments using the DR 0106EP worksheet, individuals should first determine their estimated Colorado taxable income. Then, by applying the current Colorado income tax rate of 4.63%, calculate the estimated Colorado income tax. After deducting any applicable Form 106CR credits from this amount, the net estimated tax due can be determined. This worksheet aids in calculating what should be paid each quarter, ensuring compliance with state tax requirements.

When are the estimated payments due?

Estimated tax payments for the Colorado DR 0106EP are due in four installments throughout the tax year. The first payment is due by April 15, followed by the second payment on June 15, the third payment on September 15, and the final payment on January 15 of the following year. These due dates ensure that estimated tax obligations are spread evenly across the year, helping to alleviate a large one-time tax burden.

What happens if I fail to make estimated tax payments?

Failing to make the required estimated tax payments, or making late payments, can result in an Estimated Tax Penalty. The state of Colorado calculates this penalty for each missed or late payment based on specific guidelines. However, exceptions are extended to farmers and fishermen who file and pay in full by March 1. To avoid these penalties, it’s important to adhere to the due dates and ensure that payments are made correctly and on time.

Can I make my estimated tax payments electronically?

Yes, Colorado encourages nonresident individuals to make their estimated tax payments electronically through two main methods: Revenue Online service and Electronic Funds Transfer (EFT). Both methods offer a secure and efficient means of submitting payments, with the ability to schedule payments in advance, ensuring they are received by the due dates. Pre-registration is required for EFT payments, while Revenue Online might involve a nominal processing fee. Utilizing these electronic payment options not only simplifies the process but also helps in avoiding delays and potential issues associated with paper coupons.

Filling out tax forms accurately is crucial to avoid unnecessary errors that could lead to delays or penalties. The Colorado DR 0106EP form, used for estimating taxes for nonresident composite filers, is no exception. Here are seven common mistakes made when completing this form:

Mistakes to Avoid:

Properly completing the DR 0106EP form requires careful attention to detail and a good understanding of the instructions provided. By avoiding these common mistakes, filers can help ensure their estimated tax payments for Colorado are accurate and timely, thereby avoiding potential penalties and delays.

When managing tax obligations in Colorado, especially for nonresident individuals included in a Form 106 composite filing, it's essential to be aware of other necessary forms and documents that accompany the DR 0106EP form. The completion and submission of these additional documents ensure compliance with state tax regulations and facilitate a smoother tax filing process.

Understanding and accurately completing these forms in conjunction with the DR 0106EP plays a crucial role in the tax filing process for nonresidents and entities with nonresident members. Proper documentation ensures compliance with Colorado's tax laws and can prevent penalties associated with underpayment or incorrect filing. Taxpayers should consider consulting with a tax professional to navigate the complexities of state tax requirements.

The Colorado DR 0106EP form, which pertains to 2014 Colorado Estimated Tax — Composite Nonresident Worksheet, has similarities with other forms used for estimated tax payments and composite nonresident tax filings in various jurisdictions. These resemblances include the structure, purpose, and requirements of the forms, despite differing in the specific context of Colorado's tax laws. Below are some documents similar to the DR 0106EP form and an explanation of their similarities.

Form 1040-ES, "Estimated Tax for Individuals" is utilized on a federal level for individuals to calculate and pay their estimated tax on income that is not subject to withholding, such as earnings from self-employment, interest, dividends, alimony, or rental income. Similar to the DR 0106EP, the 1040-ES includes a worksheet for calculating estimated tax payments. Both forms serve the purpose of ensuring that taxpayers meet their tax obligations on income not automatically taxed throughout the year, thereby avoiding potential penalties for underpayment.

Form NC-40, "North Carolina Individual Estimated Income Tax", closely resembles the DR 0106EP in its function for state-level estimated income tax payments. Like Colorado's form, North Carolina's version is intended for taxpayers who expect to owe tax beyond what is covered by withholding or prepaid tax. Both forms require taxpayers to estimate their income and calculate their tax obligations, breaking down payments into quarterly amounts. Each form provides specific due dates and instructions for payment submissions, emphasizing the importance of timely payments to avoid penalties.

Form IT-2105, "Estimated Income Tax Payment Voucher for Individuals" from New York serves a very similar purpose to Colorado's DR 0106EP in that it is used by individuals to submit estimated tax payments on income that is not subject to withholding. Both forms calculate payments based on estimated income and tax rates, factor in credits, and set forth a schedule of payments to ensure taxpayers meet their tax obligations throughout the fiscal year. Moreover, just like the DR 0106EP encourages electronic payments to streamline processing, the IT-2105 form also supports and sometimes recommends making payment through online systems for efficiency and security.

When it comes to filling out the Colorado DR 0106EP form, which is designed for the estimated tax for composite nonresident individuals, several best practices should be followed to ensure accuracy and compliance with state tax laws. Equally important are actions to avoid, which could lead to mistakes or penalties. Below are five recommended do's and five don'ts while working with this form.

Do:When it comes to understanding the complexities of tax forms, it's common for misconceptions to arise, particularly with forms like the Colorado DR 0106EP. Clearing up these misunderstandings is crucial to ensure that nonresident individuals and organizations fulfill their tax obligations accurately. Here are four common misconceptions about the Colorado DR 0106EP form:

Misconception 1: The DR 0106EP form is only for individual filings. This form is specifically designed for nonresident individuals who are part of a composite filing. Unlike the common belief that it's meant solely for individual use, it actually serves to streamline the process for groups of nonresident individuals included in a Composite Nonresident Return. This collective approach helps in managing tax obligations more efficiently for all parties involved.

Misconception 2: Estimated tax payments can be refunded before filing the income tax return. Estimated tax payments made using the DR 0106EP form are credits towards the taxpayer's final tax liability for the year. They cannot be refunded or otherwise returned to the taxpayer until the Colorado income tax return is filed and processed. At that point, any overpayment will be handled according to the instructions on the income tax return, either as a refund or as a credit towards future tax liabilities.

Misconception 3: Electronic payments require the DR 0106EP form to be submitted. Electronic payments do not require the submission of the physical DR 0106EP form. Taxpayers are encouraged to make payments electronically through Colorado's Revenue Online system or via Electronic Funds Transfer (EFT), which are more efficient and secure methods. These electronic options simplify the process, reducing the need for paper submissions and expediting the payment process.

Misconception 4: All nonresident individuals must make estimated tax payments. Not all nonresident individuals are required to make estimated tax payments. The obligation arises only if the individual's expected tax due, after deductions and credits, exceeds $1,000. Furthermore, the payment amount varies, as it should be the smaller of 70% of the actual Colorado tax liability, 100% of the prior year's liability for those with adjusted gross incomes of $150,000 or less ($75,000 if married filing separately), or 110% of the last year's liability otherwise. This nuanced requirement underscores the importance of accurately assessing each individual's tax situation.

Understanding these distinctions is essential for nonresident individuals participating in a composite filing and those managing their tax preparation. Accurate information helps in navigating Colorado's tax system effectively, ensuring compliance while minimizing potential issues stemming from common misunderstandings.

Understanding the Colorado DR 0106EP form is crucial for nonresident individuals who need to pay estimated taxes on Colorado-source income. Here are the key takeaways for filling out and using this form effectively:

For individuals who prefer non-electronic payment methods, the bottom part of the form serves as a payment voucher. Important to write your Colorado Account Number and "2014 Form 0106EP" on your check or money order, but do not send cash. Remember, the calculated payments and adherence to the due dates help in avoiding penalties and ensuring compliance with Colorado’s tax requirements.

Tabor 2024 Refund - Additional resources and assistance options, including FYI publications and direct support line, are noted for taxpayer convenience.

Motion to Reconsider Colorado - Designed as a two-page document to incorporate all necessary information for the legal process in eviction cases.

Transfer Car Title Colorado - The Colorado DR 2395 form is a comprehensive application for vehicle title and registration, vital for new vehicle owners in the state.