Fill a Valid Colorado 1Dr 0112Ep Form

Fill a Valid Colorado 1Dr 0112Ep Form

Navigating the intricacies of corporate tax obligations can be a daunting task for businesses in the United States, particularly when it comes to making estimated tax payments. In Colorado, the DR 0112EP form serves as a crucial tool for corporations, ensuring compliance with state tax regulations. Essentially, the form is designed to guide corporations through the process of calculating and paying their estimated taxes for the year, with the corporate tax rate set at 4.63%. It meticulously outlines the steps to determine the total estimated tax liability, taking into account any credits from the previous year or anticipated for the current year. Importantly, it sets forth the schedule for quarterly payments, emphasizing the importance of timely submissions to avoid penalties. The form further simplifies the payment process by encouraging electronic submissions, a testament to Colorado’s commitment to leveraging technology for tax administration. With detailed instructions and clear deadlines, the DR 0112EP form underscores the state’s effort to facilitate a straightforward tax-paying process for corporations. This introduction aims to shed light on the critical features and requirements of the form, ensuring Colorado corporations can fulfill their tax obligations efficiently and effectively.

DR 0112EP (11/14/13) |

|

|

|

|

|

|

COLORADO DEPARTMENT OF REVENUE |

|

|

|

|

||

Denver CO |

|

|

|

|

|

|

www.TaxColorado.com |

|

|

|

|

|

|

2014 |

Colorado Estimated Tax - Corporate |

|

|

|||

|

|

|

Worksheet |

|

|

|

|

|

|

|

|

|

|

1. |

Estimated 2014 Colorado income |

|

|

00 |

||

2. |

Recapture of prior year credits |

|

|

|

00 |

|

3. |

Total of lines 1 and 2 |

|

|

|

00 |

|

4. |

Estimated 2014 Form 112CR credits |

|

|

|

00 |

|

5. |

Colorado tax liability, line 3 minus line 4 |

|

|

00 |

||

6. |

Net estimated tax liability, line 5 times 70% |

|

|

00 |

||

Payment Number |

Net amount Due |

2013 Overpayment Applied |

Payment Due |

Due Dates |

||

|

1 |

$ |

$ |

$ |

April 15 |

|

|

|

|

|

|

|

|

|

2 |

$ |

$ |

$ |

June 15 |

|

|

|

|

|

|

|

|

|

3 |

$ |

$ |

$ |

September 15 |

|

|

|

|

|

|

|

|

|

4 |

$ |

$ |

$ |

December 15 |

|

|

|

|

|

|

|

|

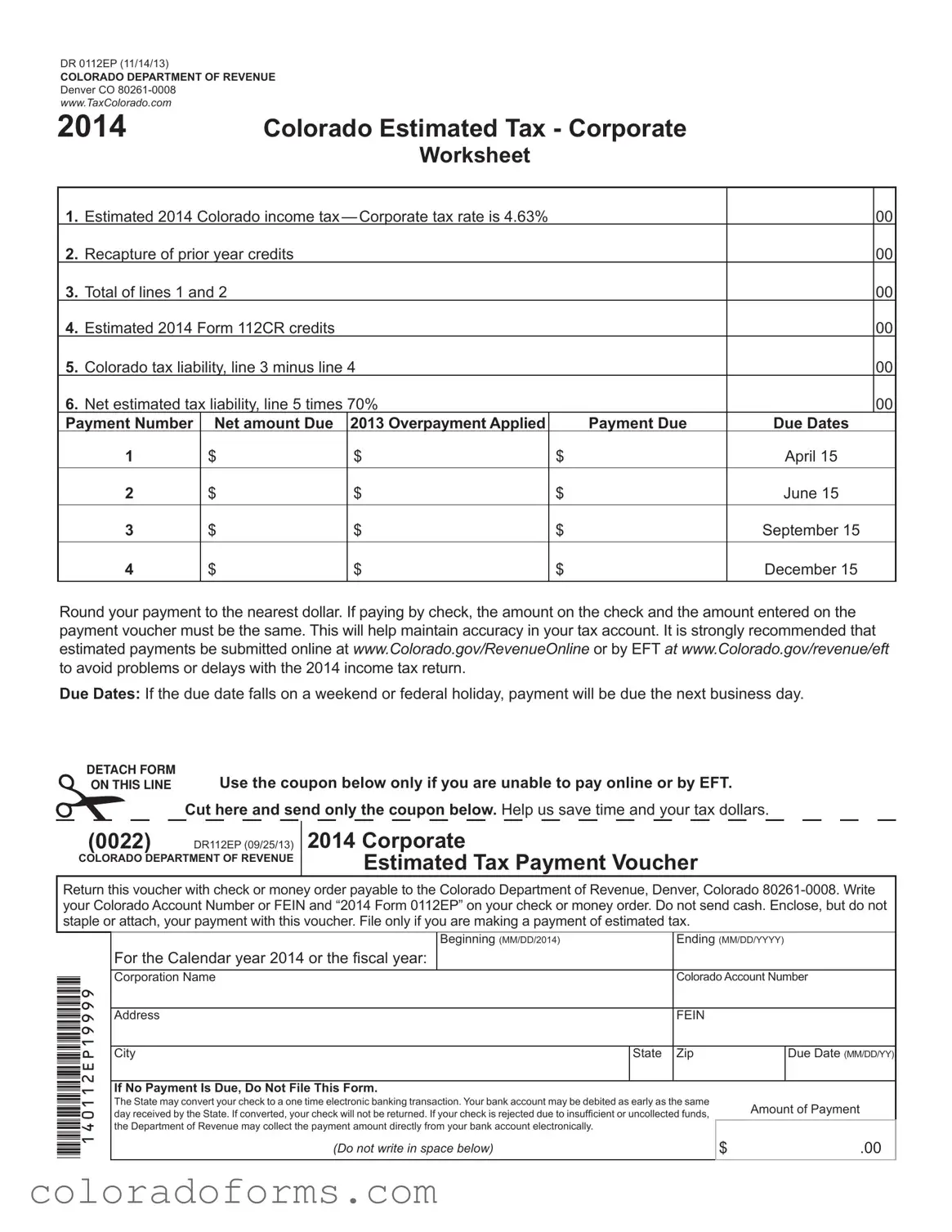

Round your payment to the nearest dollar. If paying by check, the amount on the check and the amount entered on the payment voucher must be the same. This will help maintain accuracy in your tax account. It is strongly recommended that estimated payments be submitted online at www.Colorado.gov/RevenueOnline or by EFT at www.Colorado.gov/revenue/eft to avoid problems or delays with the 2014 income tax return.

Due Dates: If the due date falls on a weekend or federal holiday, payment will be due the next business day.

DETACH FORM

ON THIS LINEUse the coupon below only if you are unable to pay online or by EFT.

Cut here and send only the coupon below. Help us save time and your tax dollars.

(0022) |

DR112EP (09/25/13) |

COLORADO DEPARTMENT OF REVENUE

2014 Corporate

Estimated Tax Payment Voucher

Return this voucher with check or money order payable to the Colorado Department of Revenue, Denver, Colorado

*140112EP19999*

|

Beginning (MM/DD/2014) |

|

Ending (MM/DD/YYYY) |

||||

For the Calendar year 2014 or the iscal year: |

|

|

|

|

|

|

|

Corporation Name |

|

Colorado Account Number |

|||||

|

|

|

|

|

|

||

Address |

|

FEIN |

|

|

|||

|

|

|

|

|

|

||

City |

State |

Zip |

|

Due Date (MM/DD/YY) |

|||

|

|

|

|

|

|

||

If No Payment Is Due, Do Not File This Form. |

|

|

|

|

|

||

The State may convert your check to a one time electronic banking transaction. Your bank account may be debited as early as the same |

Amount of Payment |

||||||

day received by the State. If converted, your check will not be returned. If your check is rejected due to insuficient or uncollected funds, |

|||||||

|

|

||||||

the Department of Revenue may collect the payment amount directly from your bank account electronically. |

|

|

|

|

|

||

(Do not write in space below) |

|

$ |

.00 |

||||

|

|

|

|

|

|

|

|

Corporate Estimated Income Tax

Instructions

See publication FYI Income 51 for more information, available at www.TaxColorado.com

General Rule

In most cases, a corporation is required to pay estimated tax if it can reasonably expect the net tax liability will exceed $5,000 for 2014. For taxpayers with a short taxable year, estimated tax payments must be remitted if the tax is expected to exceed $5,000 plus estimated credits.

Or, if a short taxable year is the result of a change in the accounting period, then income for the short period must be multiplied in a manner so that income is estimated at a full

Required Payments

The required annual amount to be paid is the smaller of:

a. 70% of the actual net Colorado tax liability.

b.100% of the preceding year’s net Colorado tax liability.

This rule only applies if the preceding year was a

*Any large corporation may base their irst quarter estimated tax payment on 25% of the tax liability from the previous year. However, the remaining payments must be based on the actual tax liability for the current year. If, after calculating the tax liability for the current year, it is determined that

the irst quarter was underestimated the shortage shall be calculated into and paid with the second quarter.

Calculating the Payment

Use the provided Worksheet to calculate the amount of estimated tax owed. Payments and forms shall be submitted using the same method (separate, consolidated, combined) and using the same account number as will be used on the annual income tax return, Form 112. If, for any reason, the

account numbers are inconsistent, the department must be notiied in writing prior to iling Form 112.

This notiication shall be mailed to:

Colorado Department of Revenue

Income Tax Section, Room 238

Denver CO

Remit payments according to the due date table provided (adjust for iscal year taxpayers). It is strongly

recommended that these payments be submitted electronically to avoid problems and delays. See the box below for details. The single form can be copied and used for each of the four quarterly payments if an electronic payment cannot be made for any reason.

Penalties

Failure to timely remit estimated tax as necessary will result

in a Estimated Tax Penalty. Penalty will be calculated for each missed or late payment. For calculation speciics,

or to remit this penalty before being billed, see Form 205, Underpayment of Corporate Estimated Tax.

Go Green with Revenue Online

Taxpayers can use www.Colorado.gov/RevenueOnline to

pay online. Online payments reduce errors and provide instant payment conirmation. Revenue Online also allows users to ile taxes, remit payments and to monitor their tax

accounts. The paper Form 0112EP or an online return is not required if an online payment is made. Please be advised that a nominal processing fee may apply to online payments.

Pay by Electronic Funds Transfer (EFT)

The EFT payment option is a free service. EFT payments can be made safely, and can be scheduled up to 12 months ahead of time to avoid forgetting to make a quarterly payment. EFT services require

Additional information, FYI publications and forms are available at www.TaxColorado.com or you may call

| Fact | Detail |

|---|---|

| Form ID | DR 0112EP |

| Issuing Authority | Colorado Department of Revenue |

| Date of Issue | November 14, 2013 |

| Purpose | 2014 Colorado Estimated Tax - Corporate Worksheet |

| Corporate Tax Rate | 4.63% |

| General Rule for Payment | Required if expected net tax liability exceeds $5,000 |

| Method of Payment Submission Recommendation | Electronically, to avoid delays or problems |

| Governing Laws | Based on section 6655 of the federal Internal Revenue Code for large corporations and specific Colorado statutes for estimated tax payments |

The task of submitting the Colorado 1DR 0112EP form is crucial for corporations to ensure compliance with the estimated tax requirements set by the Colorado Department of Revenue. This process, while it may seem daunting at first glance, can be navigated smoothly by following specific steps carefully. Given that this form plays a pivotal role in the financial responsibilities of a corporation, understanding each part of the process is imperative. Below, clear instructions are provided to assist in accurately completing and submitting the form.

After completing all required entries and calculations on the form, reviewing the accuracy of the information provided is vital before submission. Timely and precise compliance with these steps is crucial to avoid possible issues or delays with the 2014 income tax return. For corporations striving for efficiency, submitting payments electronically is strongly recommended when feasible. Doing so facilitates a more streamline process, reducing the likelihood of errors and providing instant payment confirmation. Whether opting for electronic or manual submission, understanding and adhering to these instructions is key to fulfilling the estimated tax payment obligations.

What is the Colorado DR 0112EP form?

The Colorado DR 0112EP form is a document used by corporations to calculate and pay their estimated income taxes for the year. It provides a worksheet for determining the amount of estimated tax owed, based on predicted profits and applicable tax rates. This form is crucial for corporations that expect their net tax liability to exceed $5,000 for the year.

Who is required to file the Colorado DR 0112EP form?

Corporations anticipated to have a net tax liability of over $5,000 for the tax year are required to file the Colorado DR 0112EP form. This requirement applies not only to regular tax years but also to short taxable years, including those resulting from a change in accounting periods. The form helps corporations comply with state tax regulations by making estimated payments to avoid underpayment penalties.

How do you calculate the payment due on the DR 0112EP form?

To calculate the payment due on the DR 0112EP form, corporations use the provided worksheet. It involves estimating the income tax by applying the corporate tax rate of 4.63% to the anticipated taxable income, adjusting for any applicable credits or prior year recaptures. The required payment is the lesser of 70% of the actual net Colorado tax liability or 100% of the previous year's liability, with adjustments for large corporations as specified by federal guidelines.

What are the due dates for making payments using the DR 0112EP form?

Payments using the DR 0112EP form are due quarterly, with deadlines on April 15, June 15, September 15, and December 15. If any due date falls on a weekend or federal holiday, the payment is due on the next business day. Timely payments are critical to avoid penalties for underpayment or late submission of estimated taxes.

Can payments for the DR 0112EP form be made electronically?

Yes, payments for the DR 0112EP form can and should be made electronically either through www.Colorado.gov/RevenueOnline or via EFT at www.Colorado.gov/revenue/eft. This recommendation aims to minimize errors and delays. Electronic payments offer several benefits, including instant confirmation and the ability to schedule payments in advance.

What happens if you fail to make a payment or submit the DR 0112EP form on time?

Failure to make payments or submit the DR 0112EP form by the due dates results in an Estimated Tax Penalty. Penalties are calculated for each missed or late payment. To avoid surprises, corporations should calculate and remit any penalties using Form 205, Underpayment of Corporate Estimated Tax, before being billed for them.

Are there any resources available for assistance with the DR 0112EP form?

Corporations seeking assistance with the DR 0112EP form can access numerous resources. Detailed instructions and additional information are available at www.TaxColorado.com. This website hosts relevant publications and forms, and taxpayers can also call 303-238-SERV (7378) for direct assistance. Furthermore, Colorado’s Revenue Online system offers the capability to file taxes, remit payments, and manage tax accounts conveniently online.

Filling out the Colorado 1DR 0112EP form can sometimes be confusing, leading to common mistakes. Here are some of the errors people make:

It is important to carefully follow the instructions on the form to avoid these common mistakes. By doing so, you help ensure that your estimated tax payments are processed accurately and efficiently.

When a corporation prepares its Colorado tax filings, specifically using the DR 0112EP form for estimated tax payments, several other documents may be required to complete the financial and legal obligations for the year accurately. Below is a list of other forms and documents commonly associated with the DR 0112EP form, each serving a unique purpose in the corporate tax filing process.

Understanding and utilizing these forms correctly ensures that a corporation complies with Colorado's tax laws and regulations, avoiding unnecessary penalties while leveraging available credits. Accurate completion and timely submission of these documents support a smooth tax filing process each year.

The Colorado 1Dr 0112Ep form, issued by the Colorado Department of Revenue, serves a specific purpose for corporations operating within the state. It is primarily designed for the estimation and payment of corporate income taxes that are expected to be due. This form bears similarities to other tax documents used both within Colorado and by the Internal Revenue Service (IRS) for different but related tax functions. These documents include the IRS Form 1040-ES and the Colorado Form 112.

The IRS Form 1040-ES, "Estimated Tax for Individuals," shares a functional resemblance to the Colorado DR 0112EP form. Just like the Colorado form is used by corporations to estimate and remit their income tax on a quarterly basis, the 1040-ES is utilized by individuals, including sole proprietors, partners, and S corporation shareholders, to calculate and pay their estimated taxes. Both forms require the taxpayer to predict their income for the year, calculate the estimated tax due, and make payments by set deadlines throughout the year to avoid penalties. A key similarity is the structured approach to estimating future tax liabilities and the emphasis on making periodic payments to meet tax obligations.

Similarly, Colorado Form 112, "C Corporation Income Tax Return," is related but serves a slightly different purpose. While the DR 0112EP form focuses on estimating future tax liabilities and making quarterly payments, Form 112 is for reporting the corporation’s actual income, deductions, and credits to calculate the income tax due for a fiscal or calendar year. Both forms are integral to a corporation’s tax filing responsibilities in Colorado, ensuring compliance with state tax laws. The key difference lies in their timing and function: the DR 0112EP is prospective, helping corporations to manage cash flow and avoid underpayment penalties, while Form 112 is retrospective, detailing the actual financial activity and tax liability for a past tax year.

When completing the Colorado 1DR 0112EP form for 2014 Colorado Estimated Tax - Corporate Worksheet, there are specific actions that can streamline the process, ensuring both compliance and accuracy. Below are essential do's and don'ts that corporations should consider:

By adhering to these guidelines, corporations can navigate the completion of the Colorado 1DR 0112EP form more effectively, ensuring they meet their estimated tax obligations accurately and on time. The Colorado Department of Revenue also offers additional resources and assistance through their website and contact services for those seeking further clarification or facing difficulties with their estimated tax payments.

When dealing with corporate estimated taxes in Colorado, especially concerning the DR 0112EP form, many misconceptions can lead to confusion or errors. Tackling these misunderstandings head-on can help ensure compliance and potentially save businesses from unnecessary penalties.

Misconception 1: All businesses must file the DR 0112EP form. In reality, only corporations that expect their net tax liability to exceed $5,000 for the tax year are required to make estimated tax payments using this form. This stipulation helps prevent smaller businesses from the burden of quarterly filings.

Misconception 2: Estimated payments are optional. This is not true. For those businesses that meet the criteria, estimated tax payments are not optional but a requirement. Failing to make these payments can result in an Estimated Tax Penalty, calculated for each missed or late payment.

Misconception 3: The payment method doesn't matter. While the DR 0112EP form can be filed on paper, Colorado strongly recommends electronic submission for estimated tax payments. Electronic payments can reduce errors, provide instant payment confirmation, and avoid processing delays that might occur with manual submissions.

Misconception 4: If you overestimate, you're out of luck. Some believe that if you overestimate your quarterly payments, you cannot adjust in the following quarters. However, if after calculating tax liability for the current year, it's determined that the first quarter was overestimated, adjustments can be made in subsequent payments. This flexibility helps businesses manage their cash flow more effectively.

Misconception 5: The same amount must be paid each quarter. The required payment amount can actually vary because it should be based on the smaller of 70% of the actual net Colorado tax liability for the year or 100% of the previous year’s net tax liability. This rule provides some flexibility and can help businesses adjust their payments according to their actual earnings throughout the year.

Understanding these aspects of the DR 0112EP form can help corporations navigate Colorado's tax requirements more smoothly, potentially avoiding penalties and unnecessary stress.

Understanding the Colorado 1DR 0112EP form and efficiently preparing your corporate estimated tax payments is crucial. Below are key takeaways to guide you through this process:

It's important for corporations operating in Colorado to be diligent and methodical in their approach to estimated tax payments to avoid unnecessary penalties and to take advantage of available credits. Adequate preparation and understanding of the 1DR 0112EP form lay the groundwork for a compliant and efficient tax filing process.

Tabor 2024 Refund - It’s important for businesses in Colorado to use form DR 1102 for updating or closing business details to ensure tax compliance.

Colorado State Income Tax Form - The DR 8440 ensures that all alcoholic beverages sold or manufactured in Colorado meet state standards.