Fill a Valid Colorado 104X Form

Fill a Valid Colorado 104X Form

The 2010 Form 104X, or the Amended Colorado Income Tax Return, plays a crucial role in ensuring taxpayers can correct any discrepancies in their original tax filings for the year 2010. This form allows individuals to adjust figures previously reported, including income, additions, subtractions, taxes, and credits, thereby ensuring accuracy and compliance with state tax obligations. The form is detailed, guiding taxpayers through recalculating their tax liabilities or refunds with sections dedicated to computing the amount owed or the refund due. Modifications can stem from various reasons, such as changes in federal taxable income, alterations in the taxpayer's filing status, or corrections to credits and deductions initially claimed. Taxpayers benefit from clear instructions on identifying the correct amounts for income adjustments, understanding how to determine the Colorado taxable income, and calculating the correct tax, prepayments, and credits post-amendment. For those due a refund, the form elucidates how to allocate overpayments to future estimated taxes or request a refund directly. Noteworthy is the inclusion of provisions for direct deposit refunds, accommodating for deceased taxpayers, and guidelines for part-year residents or nonresidents. Addressing statutory limitations and introducing provisions for protective claims, the form encompasses a broad spectrum of scenarios, reinforcing the importance of accuracy in tax reporting and adherence to state laws. Moreover, the form emphasizes the need for thorough documentation, urging filers to attach relevant supporting materials such as explanations of changes, corrected forms, and federal adjustments. This comprehensive approach ensures the Colorado Department of Revenue can efficiently process amended returns, maintaining the state's fiscal integrity while providing taxpayers a mechanism to rectify their tax records.

FORM 104X instRuctiOns

The 2010 Form 104X, Amended Colorado Income Tax Return, is used to correct your 2010 individual income tax return. For more information or any questions pertaining to income, additions, subtractions, credits, etc., refer to the income tax book for 2010, or call the Department of Revenue at (303)

Complete Form 104X showing the correct amounts for income, additions, subtractions, taxes and credits.

AMOunt OWED

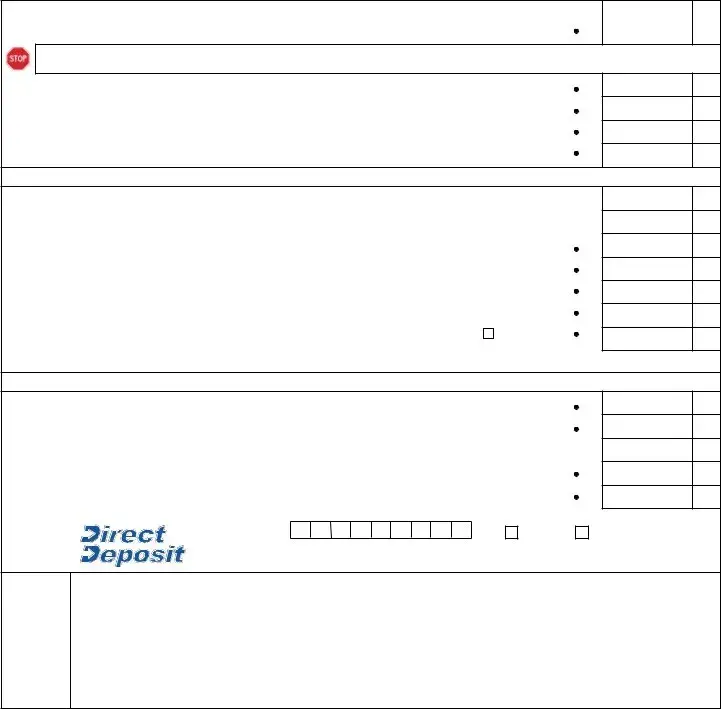

Lines 30 through 36 compute the amount owed to the state on the amended return. Any decrease in the amount of the overpayment (line 30) or increase in the amount owed (line 31) will indicate that an amount is owed with the amended return.

REFunD AMOunt

Lines 37 through 41 compute the amount of credit available on the amended return. Any increase in the amount of the overpayment (line 37) or decrease in the amount owed (line 38) will indicate that an overpayment is available with the amended return. The overpayment can be credited to estimated tax (line 40) for the tax year following the period on the amended return, or can be requested as a refund (line 41).

Attachments:

Attach an explanation of the changes to your return and, if applicable, required attachments (e.g. 104CR, DR 0204) and certiications (e.g. DR 0074). All attachments and certiications must be included with

the amended return even if there is no change to that credit or tax attribute.

copy of the federal record of account to support any changes to federal taxable income (such as a mutual fund, brokerage irm or credit union)

in the United States.

Direct Deposit:

Complete the direct deposit information if you want your refund

deposited directly into your account at a United States bank or other inancial institution.

Foreign Address:

If you are entering an address for a foreign country, use the “State” ield for the foreign country and enter the foreign postal code in the “ZIP Code” ield. A Province may be included in the “City” ield with

the city.

Deceased taxpayer:

If the taxpayer died since the original return was iled and you are

requesting a refund, attach a copy of DR 0102 — Claim for Refund

Due Deceased Taxpayer and a copy of the death certiicate. Check

the deceased box after the decedent’s name.

A federal net operating loss carried back to a tax year beginning on or after January 1, 1987, or carried forward will be allowed for Colorado income tax purposes. A nonresident or a

statute of limitations:

The statute of limitations for iling a Colorado claim for refund is generally four years from the original due date of the return or three years from the date of last payment of tax for the year involved, whichever is later.

The statute of limitations for claiming a refund that is the result of a loss

Protective claims:

If this amended return is being iled to keep the statute of limitations open pending the outcome of a court case or tax determination in

another state that affects your Colorado return, check the protective claim box under reason for iling corrected return.

Change in iling status:

If the amended return is being iled to change the iling status from single or married separate to joint, the taxpayer that iled the single return must be listed irst on the amended return. If both taxpayers have iled single, then either taxpayer can be listed irst and the explanation must specify that one of the original returns was iled

under a different primary Social Security Number (SSN).

If the amended return is being iled to change the iling status from

joint to single or married separate, the taxpayer whose SSN was

listed irst on the joint return should include all applicable tax data in

their amended return. The taxpayer whose SSN was listed second on the joint return must have an explanation that speciies the original return was iled under a different primary SSN.

interest rates on additional amounts due are as follows: |

|

January 1 through December 31, 2011. |

|

Tax due paid without billing, or paid within 30 days of billing |

3% |

Tax due paid after 30 days of billing |

6% |

Mail and make checks payable to:

colorado Department of Revenue Denver cO

FORM 104X (10/26/10)

cOLORADO DEPARtMEnt OF REvEnuE

DENVER CO

(0015) |

2010 FORM 104X |

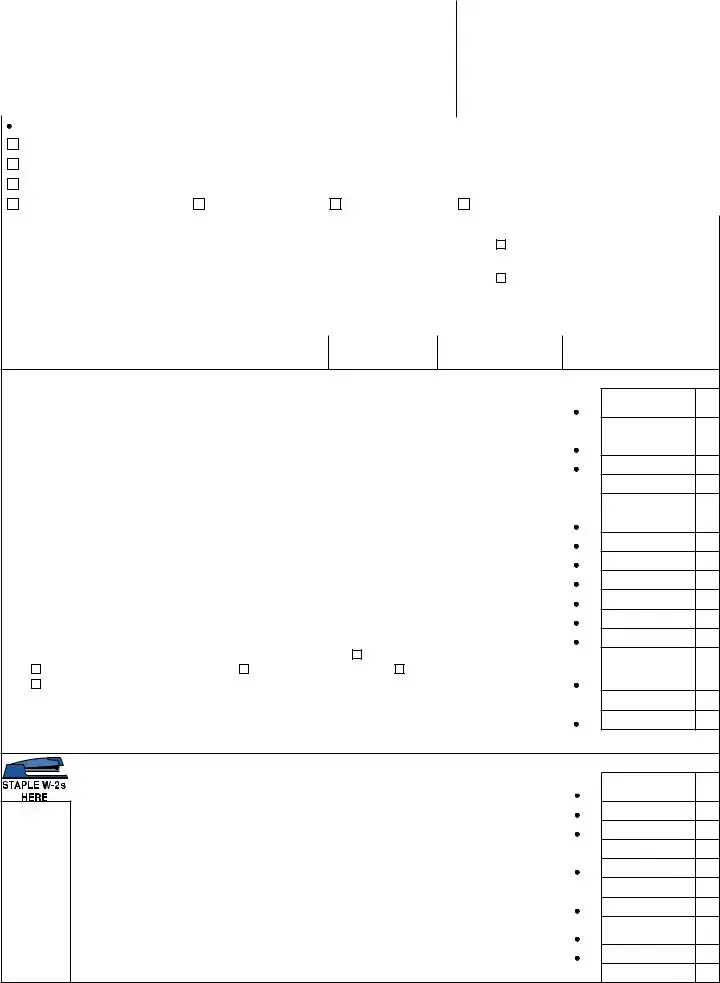

AMEnDED cOLORADO inDiviDuAL incOME tAX REtuRn

Departmental Use Only

Reason for amended return (check one): |

|

|

|

|

|

|

|

||

Investment credit carryback from tax year ending _______________________________ |

|

|

|

|

|

|

|

||

Federal net operating loss carryback fromtax year ending_________________________ |

|

|

|

|

|

|

|

||

Federal net capital loss carryback from tax year ending __________________________ |

|

|

|

|

|

|

|

||

Protective claim, attach explanation |

Other, attach explanation Changing iling status |

Changing residency status |

|

|

|

|

|||

LAst nAME |

|

FiRst nAME AnD initiAL |

|

DEcEAsED |

sOciAL sEcuRitY nuMbER |

|

|||

|

|

|

|

|

|

|

|

|

|

Yourself |

|

|

|

YEs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse, if joint |

|

|

|

YEs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address |

|

|

|

|

Your telephone number |

|

|||

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City

State

ZIP Code

AS AMENDED

1EntER AMOunt from federal Form 1040, line 43; or from federal Form 1040 A, line 27; or from federal

|

Form 1040 EZ, line 6 (Federal Taxable Income) |

1 |

ADDitiOns tO FEDERAL tAXAbLE incOME |

|

|

2 |

Enter the state income tax deduction, if any, from line 5 of Schedule A of your federal Form 1040, |

2 |

3 |

Other additions, explain: |

3 |

4 |

Total of lines 1 through 3 |

4 |

|

subtRActiOns FROM FEDERAL tAXAbLE incOME |

|

5 |

Enter the state income tax refund, if any, you reported on line 10 of your federal Form 1040 |

5 |

6 |

United States government interest |

6 |

7 |

7 |

|

8 |

8 |

|

9 |

Colorado source capital gain (5 year assets acquired on or after 5/9/94) |

9 |

10 Tuition program contribution |

10 |

|

11 |

Qualifying charitable contribution |

11 |

12 Other subtractions, see instructions and check applicable box: PERA contribution made in |

|

|

|

DPSRS contributions made in 1986; tier I or II railroad beneits; qualiied reservation income; |

|

|

wildire mitigation measures |

12 |

13 Total of lines 5 through 12 |

13 |

|

14 cOLORADO tAXAbLE incOME, line 4 minus line 13 |

14 |

|

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

GO tO tHE tAX tAbLE On PAGEs 22 AnD 23 OF tHE FORM 104 bOOKLEt WitH YOuR tAXAbLE incOME FROM LinE 14 tO FinD YOuR tAX.

stAPLE

incOME tAX, PREPAYMEnts AnD cREDits |

|

15 cOLORADO tAX from the tax table. |

|

15 |

|

16 Alternative minimum tax from Form 104AMT |

16 |

17 Recapture of prior year credits |

17 |

18 Total of lines 15 through 17 |

18 |

19 Total |

19 |

20 Net Tax, line 18 minus line 19 |

20 |

21 cOLORADO incOME tAX WitHHELD from wages and winnings |

21 |

22EstiMAtED tAX payments and credits; extension payments; and amounts withheld

on nonresident real estate sales and partnership/S corp/iduciary income |

22 |

23 Total refundable credits from line 9, Form 104CR |

23 |

24 Total of lines 21 through 23 |

24 |

AMEnDED |

|

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

25Enter the amount from federal Form 1040, line 37; or from federal Form 1040A,

line 21; or from federal Form 1040EZ, line 4 (Federal Adjusted Gross Income) |

25 |

.00

if you want the Department of Revenue to compute and mail your refund, or compute your balance due and mail a bill, stop here and leave lines 26 through 41 blank. if you want to compute the refund or balance due yourself, continue with line 26.

26 If line 24 is larger than line 20, enter your overpayment |

26 |

27 Enter the overpayment from your original return or as previously adjusted |

27 |

28 If line 20 is larger than line 24, enter the amount owed |

28 |

29 Enter the amount owed from your original return or as previously adjusted |

29 |

cOMPutE tHE AMOunt i OWE |

|

.00

.00

.00

.00

30 Line 27 minus line 26, but not less than zero |

30 |

31 Line 28 minus line 29, but not less than zero |

31 |

32 Additional tax due, total of lines 30 and 31 |

32 |

33 Interest due on additional tax |

33 |

34 Penalty due |

34 |

35 Estimated tax penalty due |

35 |

36 Payment due with this return, add lines 32 through 35 |

Paid by EFt 36 |

.00

.00

.00

.00

.00

.00

.00

The State may convert your check to a one time electronic banking transaction. Your bank account may be debited as early as the same day received by the State. If converted, your check will not

be returned. If your check is rejected due to insuficient or uncollected funds, the Department of Revenue may collect the payment amount directly from your bank account electronically.

cOMPutE YOuR REFunD |

|

|

37 Line 26 minus line 27, but not less than zero |

37 |

|

38 Line 29 minus line 28, but not less than zero |

38 |

|

39 Overpayment, total of lines 37 and 38 |

39 |

|

40 Amount you want credited to your 2011 estimated tax |

40 |

|

41 Refund claimed with this return, line 39 minus line 40 |

41 |

|

Routing number |

Type: Checking |

Savings |

.00

.00

.00

.00

.00

Account number

siGn YOuR REtuRn

Under penalties of perjury, I declare that to the best of my knowledge and belief, this return is true, correct and complete.

Your Signature |

Spouse’s Signature. If joint return, BOTH must sign. |

|||

|

|

|

|

|

Date |

|

Year of Birth |

Date |

Year of Birth |

|

|

|

|

|

|

MAiL YOuR REtuRn tO: |

Paid Preparer’s Name, Address and Telephone Number |

||

|

COLORADO DEPARTMENT OF REVENUE |

|

|

|

|

DENVER, CO |

|

|

|

|

|

|

|

|

| Fact | Detail |

|---|---|

| Purpose | The Form 104X is utilized to amend previously filed individual income tax returns for the state of Colorado, allowing corrections to be made to income, taxes, and credits reported initially. |

| Year Applicable | This specific version of the form pertains to the tax year 2010, necessitating attention to changes in tax law or financial situations retroactively. |

| Available Refunds or Amounts Owed | Recomputed amounts on the amended return can either result in owed amounts to the state or refund claims by the filer, depending on corrections made to the overpayment or tax owed figures. |

| Documentation Requirement | Filers must attach explanatory documentation for changes, as well as any relevant forms or certifications required for credits or deductions, even if no modifications to these elements are made. |

| Governing Law(s) | The filing and processing of Form 104X fall under Colorado Revised Statutes, guiding the statute of limitations for claim refunds and addressing specific considerations such as net operating losses and residency adjustments. |

Filing an amended Colorado Income Tax Return for 2010 using Form 104X is a way to correct previously submitted tax information. This might be necessary due to a change in income, deductions, or credits that affects your tax liability or refund. This detailed correction ensures your tax obligations are accurately met and may result in either additional payment to the state or a refund. To navigate this process smoothly, follow these steps and ensure all necessary documentation is attached, including any changes in federal taxable income and an explanation for the amendments. Additionally, direct deposit information can be provided for quicker processing of any potential refunds.

By following these instructions, you'll accurately amend your Colorado Income Tax Return for 2010. Ensure all relevant documentation is attached and personal information is correctly filled out to avoid processing delays. Direct deposit information will expedite any refund due.

What is the purpose of Form 104X, and when should it be used?

Form 104X, known as the Amended Colorado Income Tax Return, is designed for individuals to correct their previously filed Colorado state income tax return for the year 2010. This form is utilized when adjustments are necessary to the income, taxes, credits, or any other information reported initially, ensuring that the correct information is reflected in the state's records. It should be filed if you need to make corrections to your Colorado income tax return after it has already been filed.

How can I determine if I owe additional taxes or qualify for a refund on my amended return?

To determine if you owe additional taxes or are eligible for a refund after amending your return, review lines 30 through 36 and lines 37 through 41 on Form 104X. If there's a decrease in your overpayment or an increase in what you owe (lines 30 and 31), it indicates that you owe additional taxes. Conversely, an increase in your overpayment or a decrease in the amount owed (lines 37 and 38) signifies you may qualify for a refund. The specific amounts to be either paid or refunded can be calculated using these sections of the amended return.

What attachments are required when filing Form 104X?

When filing Form 104X, it is mandatory to include a detailed explanation of the changes being made to your return. Additionally, if applicable, you must attach all required forms and certifications, such as Form 104CR or DR 0204, even if there are no changes to those specific credits or tax attributes. For part-year residents and nonresidents, a corrected Form 104PN is required. If the amendment is due to adjustments made by the Internal Revenue Service, a copy of the federal revenue agent’s report and supporting schedules must be attached. To expedite refunds based on adjustments to federal taxable income, including a copy of the federal record of account is also advisable.

What is the statute of limitations for filing an amended return in Colorado?

The statute of limitations for filing a Colorado claim for refund typically extends four years from the original due date of the return or three years from the date the tax was last paid for the year in question, whichever comes later. However, for refunds resulting from a federal net operating loss carry-back or an investment tax credit carry-back, the statute of limitations is four aim to the due date of the return for the year in which the loss or credit originated. This timeframe is crucial for taxpayers to comply with in order to correct their return or claim a refund successfully.

When filing the Colorado 104X form, an Amended Colorado Income Tax Return, certain mistakes are commonly made. These errors can delay processing, result in incorrect computations, or even trigger audits. Understanding these mistakes can help filers avoid potential issues with their amended returns. Here are five prevalent errors:

In summarizing, when completing the Colorado 104X form, attention to detail is paramount. Mistakes can lead to delays, additional taxes owed, or incorrect refund amounts. Focusing on accurately reporting income adjustments, correctly calculating tax owed or refund due, attaching all necessary documents, accurately providing direct deposit information, and correctly noting changes in filing status or residency are critical steps in ensuring the amended return is processed efficiently and accurately.

When individuals or entities need to amend a previously filed Colorado income tax return using the Form 104X, additional forms and documents often are required to support the changes made on the amended return. This ensures the Colorado Department of Revenue can accurately review and process the modifications. Below are five forms and documents commonly used alongside Form 104X.

Proper completion and submission of these forms, when applicable, are crucial for the processing of the amended Colorado income tax return. Always ensure that each form is filled out with accurate and up-to-date information to avoid processing delays. For additional guidance on how to complete these forms or whether they apply to your situation, consider consulting the Colorado Department of Revenue's resources or a tax professional.

The Colorado 104X form is similar to the IRS Form 1040X Amended U.S. Individual Income Tax Return in several respects. Specifically, the Colorado 104X form, like its federal counterpart, the IRS Form 1040X, is designed for taxpayers who need to amend previously filed income tax returns. Both forms require the taxpayer to detail the original reported amounts alongside the corrected figures for income, deductions, and credits. Additionally, both forms calculate the difference in tax liability based on these amendments. It's this correlation in purpose—providing taxpayers with a vehicle to correct their tax returns while explaining the changes that justify the amendments—that aligns the 104X form closely with the IRS 1040X form.

Another document that shares similarities with the Colorado 104X form is the state-specific amended tax return forms from other U.S. states, such as the California Form 540X. Much like the Colorado 104X, these state-specific forms are utilized by taxpayers who seek to amend their state income tax returns due to errors, omissions, or changes in tax information after the original submission. These forms typically ask for updated information on income, deductions, tax credits, and tax payments. They also usually include sections for explaining the reasons behind the amendments, similar to the explanations required on the Colorado 104X. The consistency across these forms lies in their shared objective to rectify inaccuracies on original state tax filings, reinforcing the principle that accurate taxation is an ongoing process subject to updates and corrections.

When you're ready to fill out the Colorado 104X Form, an Amended Colorado Income Tax Return, it's crucial to ensure accuracy and compliance with state tax laws. Here’s a guide that breaks down what you should and shouldn't do:

Do:By following these dos and don'ts, you'll be better prepared to accurately complete the Colorado 104X Form and potentially avoid delays or issues with your amended tax return.

Misunderstandings often arise regarding tax forms and their requirements. The Colorado 104X form, used for amending state income tax returns, is no exception. Here are some common misconceptions:

Understanding these nuances can help taxpayers more accurately navigate the process of amending their Colorado state income tax returns, ensuring they meet their tax obligations while maximizing their potential benefits.

Filling out and using the Colorado 104X form, designed for amending individual income tax returns, can be navigated smoothly with a clear understanding of its key features and requirements. Here are some critical takeaways:

Understanding these aspects of the Colorado 104X form will help taxpayers confidently address any necessary changes to their state income tax returns, ensuring accuracy and compliance with Colorado tax laws.

Colorado 26 - Facilitates the lawful withholding and transmittal of funds from the garnishee to the creditor through detailed instructions.

Birth Certificate Colorado - It acts as a safeguard ensuring that property transactions are not undermined by clerical or informational errors, reinforcing confidence in the real estate market of Colorado.