Fill a Valid Colorado 104Pn Form

Fill a Valid Colorado 104Pn Form

For those living or earning in Colorado for only a part of the year or not at all, navigating state tax obligations can be complex. The Colorado 104PN form offers a solution, specifically designed to calculate the taxes for part-year residents and nonresidents. It's an essential document for adjusting gross income appropriately, ensuring that taxes are only paid on income earned within the state. By distilling your income into what's relevant for Colorado tax purposes, this form helps in apportioning the correct amount of tax, accounting for income from various sources such as wages, interest/dividends, unemployment benefits, and even specific adjustments like education expenses or moving costs related to moving into the state. Moreover, the form takes into consideration federal adjustments to income, with clear instructions for those who have filed different types of federal returns, including the 1040NR for nonresident aliens, ensuring that all taxpayers can accurately report their Colorado income and adjust their taxable income accordingly. Whether you're fully or partially a Colorado resident, or even a nonresident who needs to file, understanding and completing the 104PN form is a crucial step in fulfilling your state tax requirements.

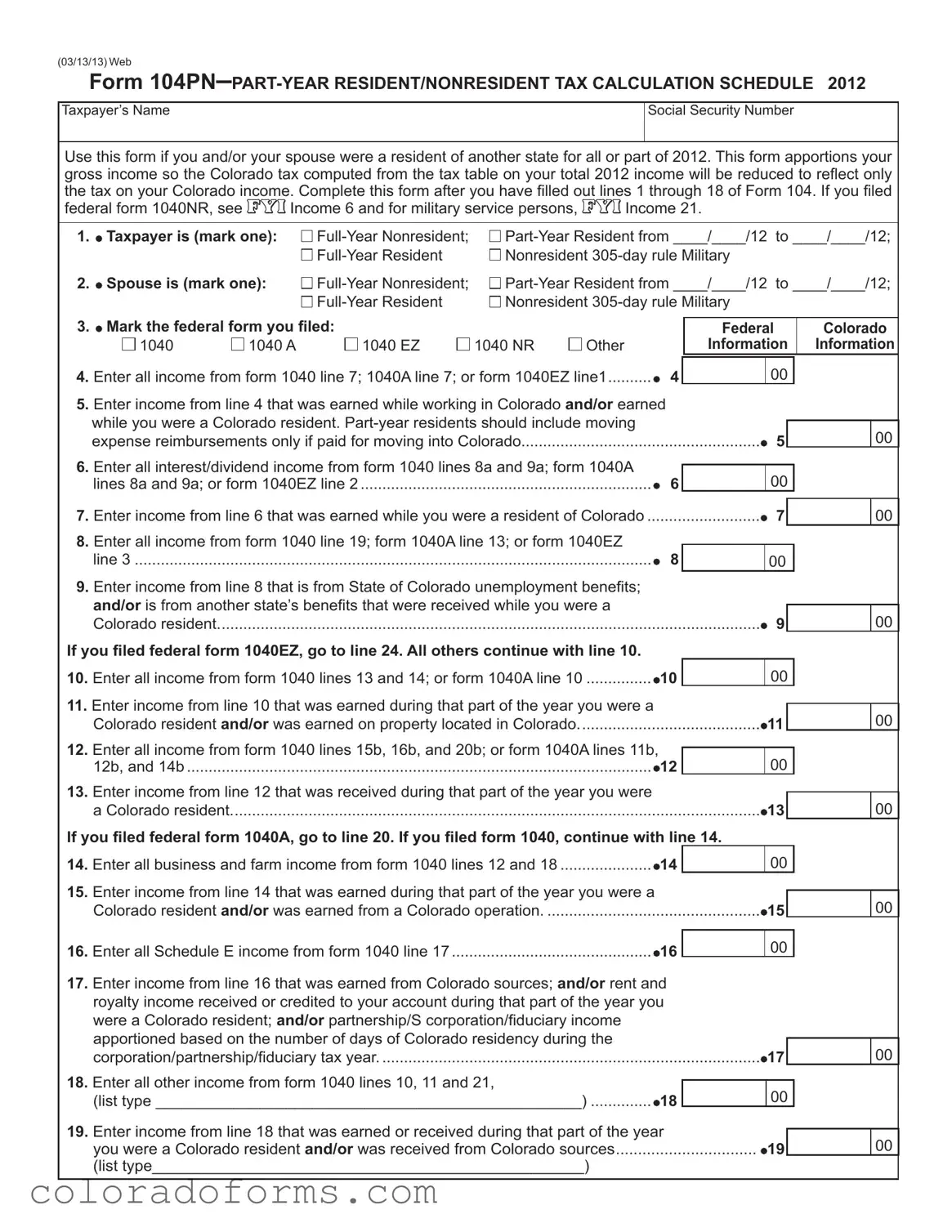

(03/13/13) Web

Form

Taxpayer’s Name

Social Security Number

Use this form if you and/or your spouse were a resident of another state for all or part of 2012. This form apportions your gross income so the Colorado tax computed from the tax table on your total 2012 income will be reduced to relect only the tax on your Colorado income. Complete this form after you have illed out lines 1 through 18 of Form 104. If you iled

federal form 1040NR, see

Income 6 and for military service persons,

Income 6 and for military service persons,

Income 21.

Income 21.

1. |

Taxpayer is (mark one): |

to ____/____/12; |

|||||||||

|

|

|

Nonresident |

|

|

|

|||||

2. |

Spouse is (mark one): |

to ____/____/12; |

|||||||||

|

|

|

Nonresident |

|

|

|

|||||

3. |

Mark the federal form you iled: |

|

|

|

|

|

|

||||

|

|

|

Federal |

|

Colorado |

||||||

|

1040 |

1040 A |

1040 EZ |

1040 NR |

Other |

|

Information |

|

Information |

||

|

|

|

|

|

|

|

|

|

|

|

|

4. Enter all income from form 1040 line 7; 1040A line 7; or form 1040EZ line1 |

4 |

|

|

00 |

|

|

|||||

5.Enter income from line 4 that was earned while working in Colorado AND/OR earned while you were a Colorado resident.

expense reimbursements only if paid for moving into Colorado |

5 |

00 |

6.Enter all interest/dividend income from form 1040 lines 8a and 9a; form 1040A

lines 8a and 9a; or form 1040EZ line 2 |

6 |

00 |

|

|

|

|

|

|

|

|

|

7. Enter income from line 6 that was earned while you were a resident of Colorado |

7 |

|

|

00 |

|

8.Enter all income from form 1040 line 19; form 1040A line 13; or form 1040EZ

line 3 |

8 |

00 |

9.Enter income from line 8 that is from State of Colorado unemployment beneits;

AND/OR is from another state’s beneits that were received while you were a

Colorado resident |

9 |

00 |

If you iled federal form 1040EZ, go to line 24. All others continue with line 10.

...............10. Enter all income from form 1040 lines 13 and 14; or form 1040A line 10 |

10 |

|

00 |

11.Enter income from line 10 that was earned during that part of the year you were a

Colorado resident AND/OR was earned on property located in Colorado |

11 |

00 |

12.Enter all income from form 1040 lines 15b, 16b, and 20b; or form 1040A lines 11b,

12b, and 14b |

12 |

00 |

13.Enter income from line 12 that was received during that part of the year you were

a Colorado resident |

13 |

00 |

If you iled federal form 1040A, go to line 20. If you iled form 1040, continue with line 14.

.....................14. Enter all business and farm income from form 1040 lines 12 and 18 |

14 |

|

00 |

15.Enter income from line 14 that was earned during that part of the year you were a

Colorado resident AND/OR was earned from a Colorado operation. |

................................................. |

15 |

|

00 |

|

16. Enter all Schedule E income from form 1040 line 17 |

16 |

|

|

|

|

|

00 |

|

|||

17.Enter income from line 16 that was earned from Colorado sources; AND/OR rent and royalty income received or credited to your account during that part of the year you

were a Colorado resident; AND/OR partnership/S corporation/iduciary income |

|

|

apportioned based on the number of days of Colorado residency during the |

17 |

|

corporation/partnership/iduciary tax year |

00 |

18.Enter all other income from form 1040 lines 10, 11 and 21,

(list type _________________________________________________) |

18 |

00 |

19.Enter income from line 18 that was earned or received during that part of the year

you were a Colorado resident AND/OR was received from Colorado sources |

19 |

00 |

(list type_________________________________________________) |

|

|

|

|

Federal |

Colorado |

|

|

|

Information |

Information |

|

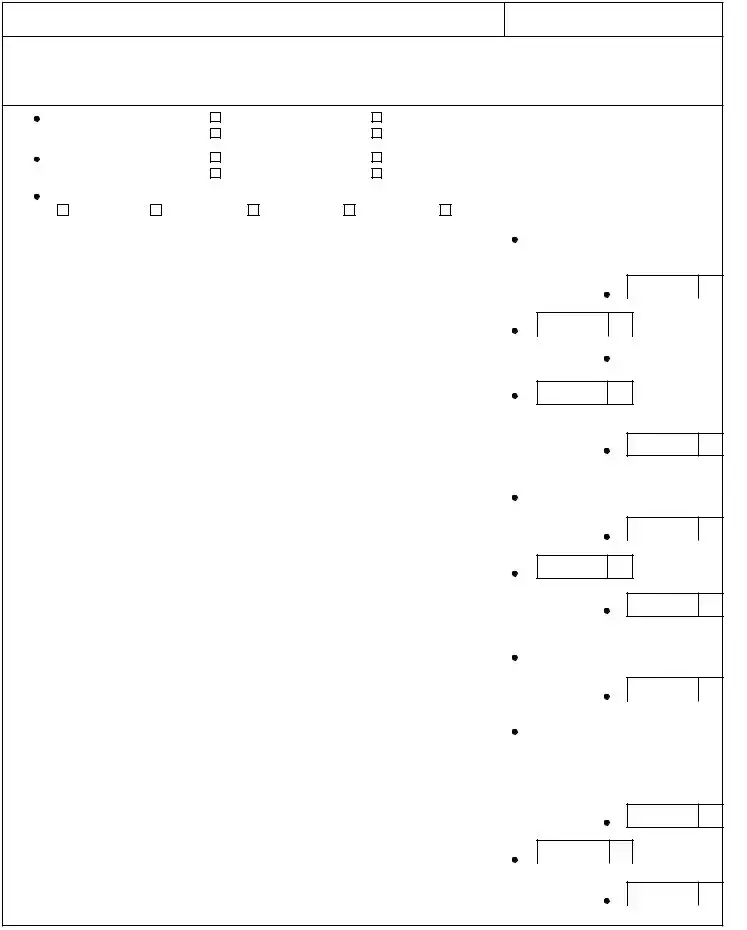

20. Total Income. Enter amount from form 1040 line 22; or form 1040A line 15 |

20 |

|

|

|

|

00 |

|

||

21.Total Colorado Income. Enter the total from the Colorado column, lines 5, 7, 9, 11,

13, 15, 17 and 19 |

21 |

00 |

22.Enter all federal adjustments from form 1040 line 36, or form 1040A line 20

(list type______________________________________________________) .. |

22 |

00 |

|

|

23. Enter adjustments from line 22 as follows: (list type_____________________) |

23 |

|

|

|

|

00 |

|||

•Educator expenses, IRA deduction, business expenses of reservists, performing artists and

in the ratio of Colorado wages and/or

•Student loan interest deduction, alimony, and tuition and fees deduction are allowed

in the Colorado to federal total income ratio (line 21/ line 20).

•Domestic production activities deduction is allowed in the Colorado to Federal QPAI ratio.

•Penalty paid on early withdrawals made while a Colorado resident.

•Moving expenses if you are moving into Colorado, not if you are moving out.

•For treatment of other adjustments reported on form 1040 line 36, see

Income 6.

Income 6.

24.Adjusted Gross Income. Enter amount from form 1040 line 37; or form 1040A line 21;

or form 1040EZ line 4 |

24 |

00 |

25.Colorado Adjusted Gross Income. If you iled form 1040 or 1040A, subtract the amount on line 23 of Form 104PN from the amount on line 21 of Form 104PN . If you

iled form 1040EZ, enter the total of lines 5, 7 and 9 of Form 104PN |

25 |

26.Additions to Adjusted Gross Income. Enter the amount from line 3 of Colorado

Form 104 excluding any charitable contribution adjustments |

26 |

00 |

27.Additions to Colorado Adjusted Gross Income. Enter any amount from line 26 that is

from

AND/OR any

|

a Colorado resident. (See |

Income 6 for treatment of other additions) |

.................................. |

27 |

28. |

Total of lines 24 and 26 |

28 |

00 |

|

29. |

Total of lines 25 and 27 |

|

29 |

|

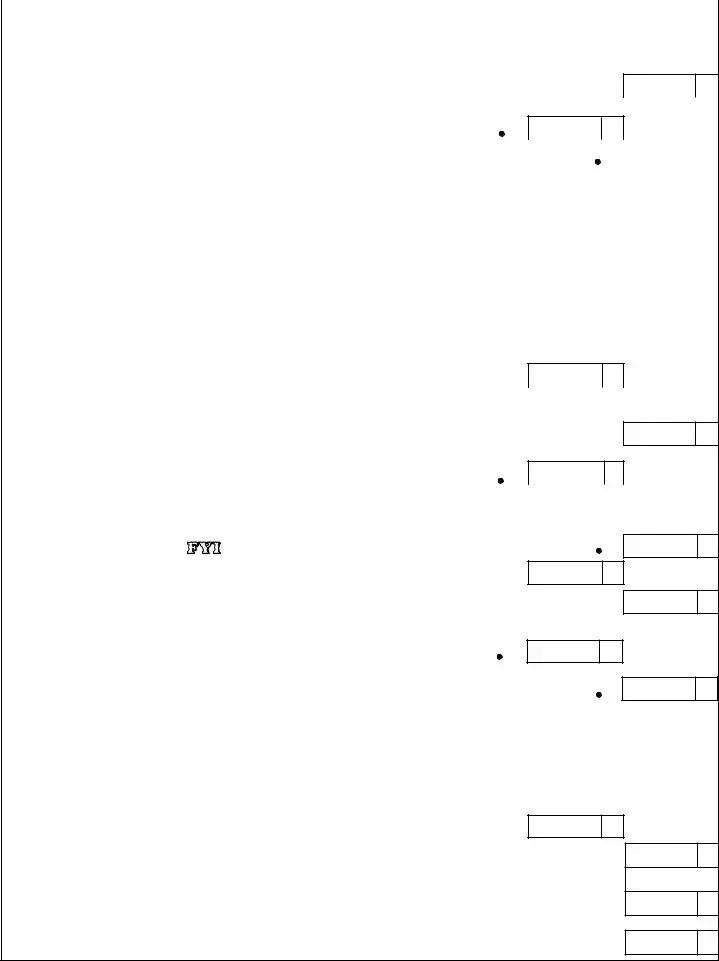

30.Subtractions from Adjusted Gross Income. Enter the amount from line 17 of Colorado

Form 104 excluding any qualifying charitable contributions |

30 |

00 |

31.Subtractions from Colorado Adjusted Gross Income. Enter any amount from line 30

as follows: |

31 |

•The state income tax refund subtraction to the extent included on line 19 above,

•The federal interest subtraction to the extent included on line 7 above,

•The pension/annuity subtraction and the PERA or School District Number One retirement subtraction to the extent included on line 13 above,

•The Colorado capital gain subtraction to the extent included on line 11 above,

•For treatment of other subtractions, see

Income 6.

Income 6.

32.Modiied Adjusted Gross Income. Subtract the amount on line 30 from the amount

on line 28 |

32 |

00 |

00

00

00

00

33.Modiied Colorado Adjusted Gross Income. Subtract the amount on line 31 from the

|

amount on line 29 |

33 |

34. |

Amount on line 33 divided by the amount on line 32 |

34 |

35. |

Tax from the tax table based on income reported on Colorado Form 104 line 18 |

35 |

36. |

Apportioned tax. Amount on line 35 multiplied by the percentage on line 34. Enter |

|

|

here and on Form 104 line 19 |

36 |

00

%

00

00

| Fact | Detail |

|---|---|

| Form Type | Web Form 104PN–PART-YEAR RESIDENT/NONRESIDENT TAX CALCULATION SCHEDULE |

| Release Date | March 13, 2013 |

| Intended Users | Taxpayers who were residents of another state for all or part of the preceding year |

| Purpose | To apportion income so that Colorado tax is calculated only on Colorado income |

| Governing Law | Colorado State Tax Law |

| Key Features | Includes specific lines for different income types and corresponding adjustments for part-year and non-residents |

Filling out the Colorado 104PN form is crucial for residents and non-residents who have earned income in Colorado. This form helps apportion your income, allowing the state to tax you only on the income earned within Colorado. It's important to complete this form accurately to ensure that your tax obligations are met correctly. Below are step-by-step instructions for completing the form, designed to guide you through each section smoothly and efficiently.

By meticulously following these steps, you ensure your Colorado income tax reflects only the income earned within the state, potentially lowering your tax obligation compared to a straightforward calculation without this apportionment. Remember, accuracy in reporting and adherence to the instructions can help avoid processing delays or issues with your tax return.

What is the purpose of Form 104PN?

Form 104PN is designed for individuals who were residents of another state for all or part of the tax year. It helps apportion the taxpayer's gross income, allowing the Colorado tax liability to reflect only the income earned from sources within Colorado. This is achieved by adjusting the state tax based on the proportion of Colorado income to total income.

Who needs to file Form 104PN?

Individuals who were part-year residents or nonresidents of Colorado and had income from Colorado sources need to file Form 104PN. This includes those who moved to or from Colorado during the tax year, nonresidents with income from a Colorado operation, and military personnel who meet certain criteria.

How do I determine if I was a part-year resident or nonresident?

You are considered a part-year resident if you moved to Colorado during the tax year and established domicile, or if you moved out of Colorado and established domicile in another state. Nonresidents are individuals who did not establish domicile in Colorado but earned income from Colorado sources.

Do I need to file Form 104PN if I filed federal form 1040NR?

Yes, individuals who filed federal form 1040NR and had income from Colorado sources are required to file Form 104PN. The form is necessary to calculate the portion of income tax due to Colorado.

What income should be included on line 5 of Form 104PN?

On line 5, you should include all income earned from working in Colorado and/or income earned while a Colorado resident. For part-year residents, this includes moving expense reimbursements if the move was into Colorado.

How is "Total Colorado Income" on line 21 calculated?

Total Colorado Income on line 21 is the sum of the income from Colorado sources listed on lines 5, 7, 9, 11, 13, 15, 17, and 19. This figure represents the income subject to Colorado state tax.

What adjustments are allowed for Colorado Adjusted Gross Income?

Adjustments to your Colorado Adjusted Gross Income include a portion of federal adjustments such as educator expenses, IRA deductions, business expenses for certain professionals, health savings account deductions, and self-employment tax deductions, among others. These are allowed in proportion to the ratio of Colorado income to total income.

Are there any specific deductions for military service members?

Military service members can deduct income related to military service that meets specific criteria outlined in the instructions for Income 21 on the form. This may include certain exclusions for military pay or benefits.

How do I calculate the apportioned tax due to Colorado?

The apportioned tax due to Colorado is calculated by applying the percentage of Colorado income to total income (line 34) to the tax determined from the tax table based on income reported on Colorado Form 104 line 18. This amount is then reported on Form 104 line 19.

What steps should I follow if I filed a form other than 1040, 1040A, or 1040EZ?

If you filed a federal tax form other than 1040, 1040A, or 1040EZ, you should follow the specific instructions provided in the Form 104PN for reporting income and making necessary adjustments. The same principles of apportioning income to reflect Colorado sources apply, but adjustments may need to be tailored to the specific lines and items of your filed form.

Filling out tax forms can be tricky, and the Colorado 104PN Form is no exception. This form, designed for part-year residents or nonresidents who need to calculate their Colorado tax obligations, often trips up taxpayers. Below are seven common mistakes to avoid to ensure accurate and compliant tax filings.

When tackling the 104PN Form, taking care to avoid these pitfalls can save taxpayers from both unintended underpayments and the hassle of amending forms later. It's always advisable to consult with a tax professional if you are unsure about how to properly fill out this form or have complex tax situations.

When dealing with taxes, especially when filing with specific state requirements like the Colorado 104PN form, it's important to have all necessary documents at hand. This form, used for part-year residents and nonresidents to calculate their Colorado tax obligations, may require additional documentation to fully support the tax calculations presented.

Each document serves a particular purpose in ensuring the accuracy and completeness of your tax filings. Keeping these records organized can significantly streamline the process of filing your Colorado 104PN form and other related tax forms. Remember, careful documentation is key to accurately determining your tax obligations and ensuring compliance with state and federal laws.

The Colorado 104Pn form, designed for part-year residents and nonresidents to calculate their state tax obligation, shares resemblances with several other tax documentation processes across the United States. Although unique to Colorado, its structure and purpose mirror those of forms like California's 540NR and New York's IT-203, which serve similar functions for individuals in those states who need to apportion their income based on residency status. Each of these documents requires taxpayers to distinguish income earned within the state from their total income, ensuring that they are taxed only on the income attributable to the state in question.

Specifically, the form closely aligns with California's 540NR Nonresident or Part-Year Resident Income Tax Return. Both necessitate the differentiation of in-state from out-of-state earnings, allowing part-year residents and nonresidents to calculate state-specific tax liability accurately. They cater to individuals who have moved into or out of the state within the fiscal year or have income sources across state lines. By compartmentalizing income and deductions based on residency, these forms prevent double taxation and ascertain that taxpayers contribute their fair share based on the time spent within each state's borders.

Similarly, New York's IT-203 form, Nonresident and Part-Year Resident Income Tax Return, parallels the Colorado 104Pn form in its approach to income apportionment. Both demand detailed income reporting and adjustments specific to the state's tax laws, factoring in various incomes, such as wages, interests, dividends, and capital gains, based on their source location. This process ensures equitable tax treatment for individuals who live out of state for part of the year or earn money from multiple states, underpinning the broader objective of aligning tax obligations with individuals' actual ties to the state.

In conclusion, while the Colorado 104Pn form is tailored to meet the specific needs of Colorado's tax system, its foundational principles of income apportionment and residency-based taxation are reflected across various states' tax codes. By looking at the similarities between the Colorado form and those of other states, we gain insight into the common challenges and solutions faced by part-year residents and nonresidents in navigating the complexities of state taxation in the United States.

Understanding how to properly fill out the Colorado 104PN form is crucial for part-year residents and nonresidents who need to calculate their state tax obligations accurately. Here are ten essential dos and don'ts to ensure the process is flawless.

Dos:

Double-check that the 104PN form is the correct form for your situation, particularly if you were a part-year resident or a nonresident with Colorado source income in 2012.

Complete lines 1 through 18 of Form 104 before starting the 104PN form, as this will provide necessary information for accurate tax calculation.

Accurately mark your residency status and the residency status of your spouse, if applicable, to ensure correct tax treatment.

Report all income accurately, including wages, interest/dividends, and any other earnings, focusing on those sourced from Colorado.

Remember to include income from Colorado state unemployment benefits, or if you received benefits from another state while you were a Colorado resident.

Calculate adjustments accurately, following guidance for specific deductions and how they are apportioned based on Colorado income.

Ensure all federal adjustments are reported correctly, as these can impact your Colorado tax calculation.

Review the treatment of additions and subtractions to adjusted gross income specific to Colorado, especially if you have out-of-state income, to not miss any beneficial subtractions.

Use the correct line references from your federal tax forms to ensure the information transferred to the 104PN form is accurate.

Sign and date the form upon completion, as an unsigned form can lead to processing delays or be considered invalid.

Don'ts:

Do not guess your residency status—make sure to understand the definitions for full-year resident, part-year resident, and nonresident as they relate to your situation.

Avoid skipping entries for moving expenses. For part-year residents, include reimbursements only if for moving into Colorado.

Do not include income that was not earned from Colorado sources unless specifically required for your residency status.

Refrain from overlooking interest/dividend income and unemployment benefits that are subject to state taxes.

Don't miss adding back certain federal adjustments to income that don't apply to your Colorado income, as this could lead to underreported income.

Avoid making errors in calculating the ratio of Colorado income to total income, which is necessary for some deductions and credits.

Don't forget to consider each type of income and adjustment for its specific treatment under Colorado tax laws.

Avoid submitting the form without reviewing it for completeness and accuracy to avoid potential issues with your tax return.

Do not overlook the need to attach this form to your Colorado tax return if you are filing by paper.

Finally, don't miss the filing deadline, as late submissions can result in penalties and interest charges.

By following these guidelines, taxpayers can avoid common errors and ensure their Colorado 104PN form is filled out correctly, leading to an accurate state tax calculation.

When navigating the complexities of state tax forms, individuals often come across misunderstandings that can complicate the filing process. The Colorado 104PN form, vital for part-year residents and nonresidents calculating their state tax liabilities, is no exception. Let's address and correct some of the most common misconceptions about this form.

Everyone must file the 104PN form: Not true. Only those who were part-year residents or nonresidents of Colorado during the tax year need to complete this form. It is specifically designed to apportion income to Colorado for tax purposes.

The 104PN form can be used for any tax year: Incorrect. The form is updated annually to reflect the current tax laws and regulations. Ensure you're using the version specific to the tax year for which you are filing.

If you didn't earn income in Colorado, you don't need this form: This is a misconception. Part-year residents and nonresidents may still need to file the form to report any income, deductions, and credits proportionate to their time in Colorado.

Military income is not reported on the 104PN form: This is incorrect. Military personnel need to follow specific guidelines outlined in Income 21 on the form, which details how to report military income or adjustments.

You need to itemize deductions on the 104PN form: Not necessarily. The form is used to calculate Colorado income and does not itself require itemization of deductions. However, federal adjustments are necessary and can affect the Colorado adjustments.

Filing a federal return exempts you from the 104PN: Filing a federal return does not exempt individuals from completing the 104PN if they were part-year residents or nonresidents with Colorado income. The state form is independent of the federal return, serving different purposes.

Nonresidents don't owe Colorado taxes: False. Nonresidents who earned income from Colorado sources are required to file the 104PN to calculate taxes owed to the state on that income.

The 104PN calculates your total tax liability: Misleading. The 104PN helps determine the portion of your income taxable by Colorado. Your total tax liability is determined after applying this calculation to the broader tax return.

There are no adjustments for part-year residents: Incorrect. Part-year residents can make adjustments on their 104PN forms to reflect the portion of income earned while they were residents of Colorado.

Completing the 104PN guarantees no audit: Filing this form accurately and according to guidelines can help ensure compliance with Colorado tax laws, but it does not guarantee avoidance of an audit. Audits can be triggered by a variety of factors unrelated to the 104PN form itself.

Understanding the purpose and requirements of the Colorado 104PN form can significantly ease the tax filing process for those who lived in or earned income from Colorado sources during a part of the tax year. Clearing up these misconceptions is the first step toward accurate and stress-free tax reporting.

Filling out the Colorado 104PN form is essential for part-year residents and nonresidents who have earned income in Colorado. This form allows you to accurately calculate your tax obligations based on income earned in the state. Understanding the key components and instructions can simplify the process and ensure you meet your tax responsibilities effectively. Here are some key takeaways to guide you through filling out and using the Colorado 104PN form:

To accurately complete your Colorado 104PN form, review each instruction carefully and verify all information related to your residency and income sources within Colorado. Ensuring accuracy in these areas will lead to a correct tax calculation, reflecting only your tax liability for income earned within the state.

What Is Tax Exempt Certificate - A Colorado state form specifically for contractors to obtain tax exemptions on materials for eligible construction projects.

Colorado Driver's License Veteran Designation - Offers a legal exemption from specific ownership taxes for vehicles of military members based in Colorado.

Colorado Payroll Tax Registration - The option to apply online for licenses through the CR0100 form represents a convenient pathway for businesses to quickly achieve compliance while saving time.